There is much to make sense of to our common sense of the morality of forever money in the accounting for expected fturue cash flows through Enterrpise as a social reactor for transforming cost-for-value into value-for-price.

The details will always be different for every Enterprise (and the devil is always in those details), but at a high level, where impacts on people and planet can be centered, a standard Chart of Accounts can be designed that can be taken as a starting point for every Enterprise, specifically for the prupose of facilitating comparative analysis of diverse Enterprises through the fiduciary lenses of Prudence and Loyalty.

To start the processing of agreeing on standards, consider the following:

- Stewardship of Revenues

- Good Stuff for People and Planet, throughout the population and across the generations, now and in the future

- Stuff that is Not Good for People and Planet, harmful to population across the generations, now and in the fiture

- Stewardship of Trade, with suppliers

- Energy

- Materials

- Assemblies and Sub-Assemblies

- Inventory Acquired for Resale (in GAAP: Cost Of Goods Sold)

- Stewardship of Engagement, with communities, of place, and of interest

- Industry

- Government

- Community

- Stewardship of Reckoning, with the consequnces, on Nature, on Society and on our shared future

- Habitat Vitality

- Social Equity

- Future Caring

- Stewardship of Working, in the workplace

- Wages and Hours

- Benefits

- Working Conditions

- Stewardship of Dealing, in the marketplace

- Customers (product safety, truth-in-advertising, and such)

- Competitors

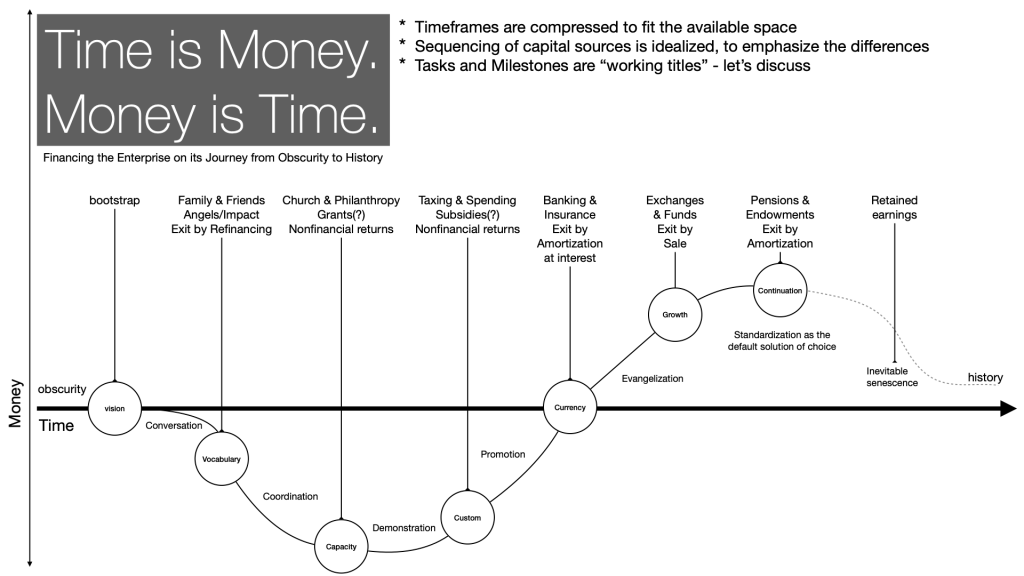

- Stewardship of Sharing, with the savers whose savings are the “raw material” that Finance transforms into capital for business

- savings as money set aside to provide for our own, aggregated through Family & Friends, and allocated as capital for business through the financial mathematics of patronage for IMPACT

- savings as money set aside to provide for others, aggregated through Church & Philanthropy, and allocated as capital for business through the financial mathematics of grants for MISSION

- savings as money set aside to contribute to the costs of public health, public safety and the public wellbeing, aggregated through Taxing & Spending, and allocated as capital for business through the financial mathematics of subsidies for POLICY

- savings as money set aside to safekeeping and future transacting, aggregated through Banking & Insurance, and allocated as capital for business through the financial mathematics of monetization of PROPERTY

- savings as money set aside to idiosyncratically put money to work making more money, opportunistically, aggregated through Exchanges & Funds, and allocated as capital for business through the financial mathematics of profit extraction from SELLING PRICE

- savings as money set aside to provide to programmatically provide certainty against certain of life’s future financial uncertainties through Pensions & Endowments, and allocated as capital for business through the financial mathematics of capacity for AIMS.

A New View of Financing for Enterprise

Standard accounting (in the US, GAAP) is designed to show a lender a snapshot of profitability, liquidity, seasonality and capital adequacy/collateral value.

These are the metrics by which a lender gauges their confidence in a loan.

If profitability, liquidity and debt-to-equity ratios are robust, the lender feels secure.

If profitability, liquidity and ratios are wavering, erratic and diminishing, the lender begins to feel insecure. The loan is put on a watch list, and the lender begins to prepare to action to protect itself in case the loan fails.

The securities trading markets have adapted the debt metrics of income statesment sand balance sheets to support so-called fundamental analysis of anticipated changes in market clearing prices for bonds (debt) and stock (equity), caclulating historical growth trends, which are then project forward into the future, as a fundamental predictor of future market price movements.

There is a lot more going on in what actually derives price movements in the securities trading markets along the emotional rollercoarster of buy-low-to-sell-high, but this grounds the chaos in some vestige of rationality.

Out of which gossamer theads, Economists weave fables of rational self-interest and efficiency in price discovery.

“Mirroring in Latin is speculatus. … The idea is you create a distance between you and yourself and you reflect on your behavior by looking at yourself in this mirror which, in accounting terms, is the financial reports that are produced at the end of the year, or when you close the books and you open them again. Interestingly, this speculation was a moment of reflection, a moment of reflecting on your morality. In modern times, this has devolved into a degraded sense of speculation, however. “I don’t even care about who I am and why I’m here, I just want to make money.”

THE METAPHYSICS OF ACCOUNTING WITH PAOLO QUATTRONE

by Money on the Left

https://moneyontheleft.org/2021/12/01/the-metaphysics-of-accounting-with-paolo-quattrone%EF%BF%BC/There is not a lot that makes sense to our common sense about these mythical tales free market rationality.

Which is why, when we made the mistake, back in the 1970s, of allowing forever money to flow into the economy through the securities tradign markets, we cut off all accountability of fiduciary stewardshop to plain common sense.

“The investment professionals have basically pushed out the attorneys from interpreting fiduciary duty”

– Keith Johnson

https://gailnet.org/events/fiduciary-duties-23-june-2022/

@ 6:11

We cannot