Pensions Are Powerful

People Power Pensions

Shouldn’t people have the power?

– Matt Orsagh, Arketa Institute

What is the capacity that Pensions & Endowments derive from their character as large, programmatic and self-perpetuating “forever machines’, under the circumstances now prevailing?

People

Taking Back Our Power,

through

Citizens’ Deliberations

Tens of trillions in society’s shared savings are aggregated, collectively, worldwide, into self-perpetuating social trusts for programmatically provisioning mutual aid societies for Workforce Pensions.

Additional trillions are aggregated to endow Universities, Foundations and other Civil Society Institutions.

These trusts are special, because they are, truly, “forever machines”. Their purpose is to keep themsevles ongoing. Also, they are fiduciary. They are constrained by the law of fiduciary duty, which are remarkably uniform in jurisdictions around the world, to act in undivided loyalty to their legally constituted purpose, of keeping themselves ongoing, for a purpose.

Further, they are accountable for compliance with their duties by a standard of evidence sometimes called in the law The Hypothetical Reasonable Person, as an avatar for our shared common sense of what makes sense, as prudent people who care enough to take the time to make the effort to make ourselves familair with such matters.

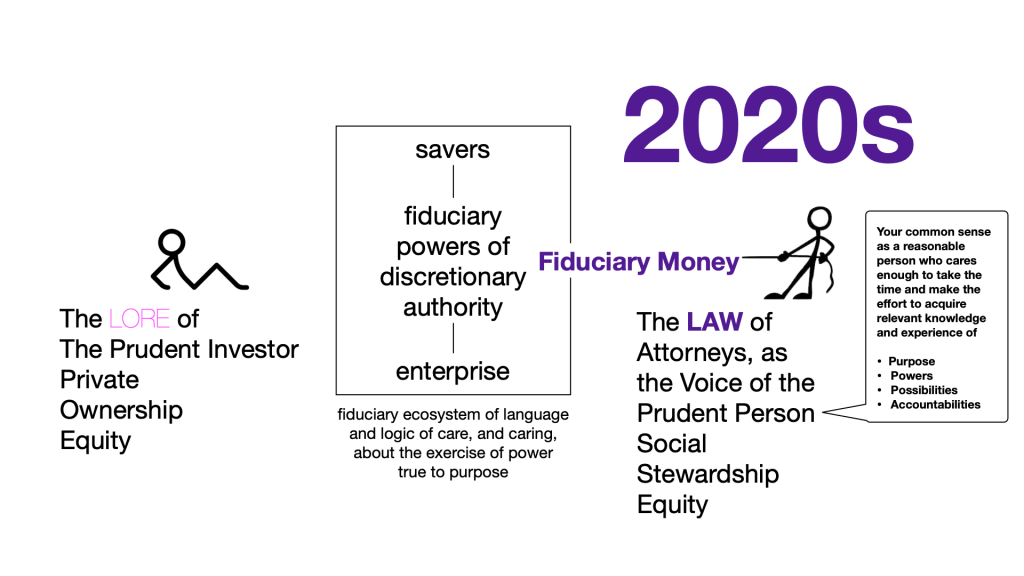

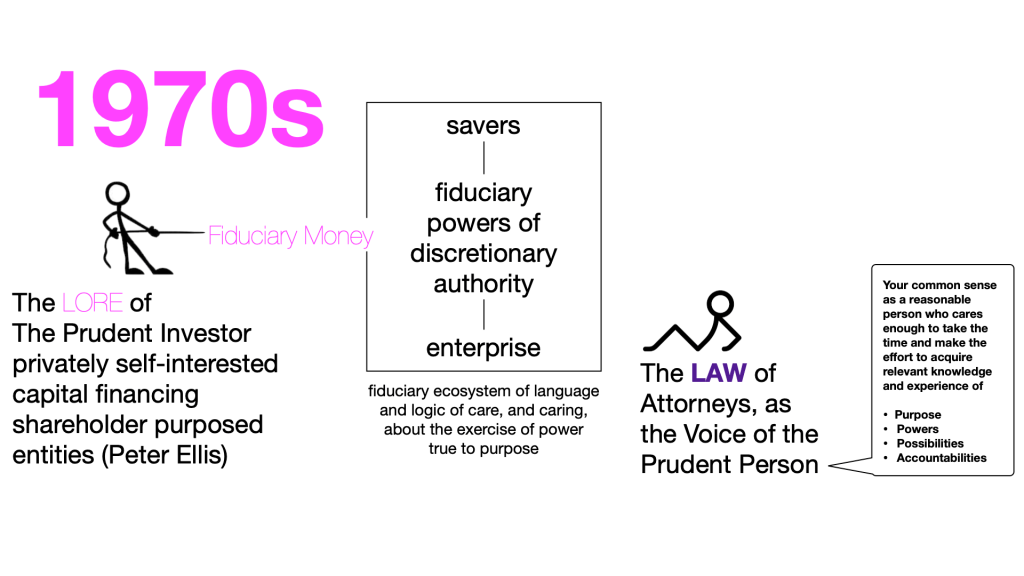

Who is the Hypothetical Prudent Person?

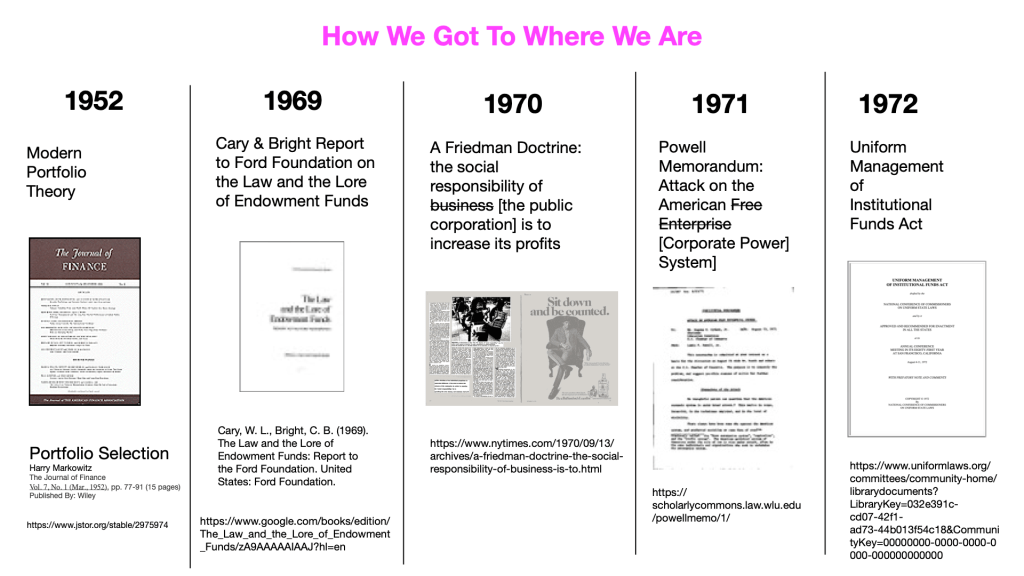

We haven’t considered, in public discourse, guided by legal experts, the power of Pensions & Endowments to allocate the aggregations we entrust to their plenary powers of discretionary authority since the early 1970s, when Modern Portfolio Theory was recognized as an update, and an upgrade, to the capacity Pensions & Endowments derive from their character, under the circumstances then prevailing.

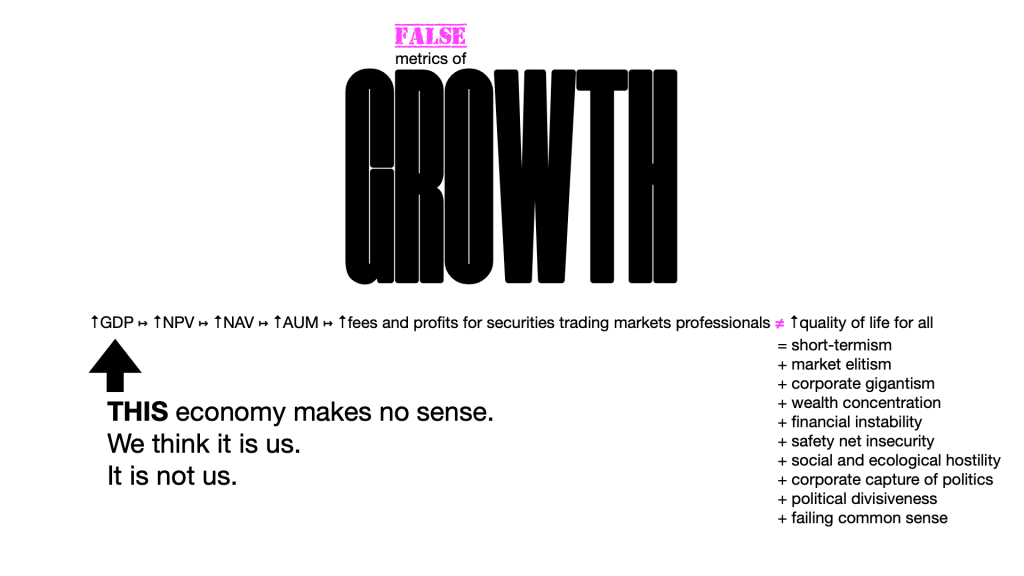

What we did not realize at the time, was the way in which this update and upgrade effectively shackles to a locked imaginary that Growth, as the simple, quantitative increase in transaction volumes measured in numbers, as prices paid in money, from one period of measurement to the next, is both necessary and suffcient to our being and our wellbeing, as Humans on Earth.

It also prevented us from seeing the new update and upgrade to the capacity of Pensions & Endowments made possible by the invention of personal computing, and the knowledge and information technologies of spreadsheet math, desktop publishing and digital communication, in the 1980s.

To this very day, we have not yet upgraded our common sense of the capacity that these personal computing technologies give Pensions & Endowments, to use those technologies to allocate the aggregations we entrust to their plenary powers of discretionary authority through a new financial mathematics of amortization to an actuarial/fiduciary cost of money, plus oppportunistic upside, from cash flowing through Enterprise that is prioritized by contract for:

- Suitability of the technology choices being made available to popular choice through the Enterprise, to the circumstances prevailing at the time;

- Duration of the social conract between the Enteprise and Popular Choice, regarding the fitness-for-purpose, price-for-performance, availability and abilty-to-pay, of those technology choices, over time; and

- Dignity in how the business does its business of making those choices available to popular choice, all the time, showing us six vectors of cash flow through enterprise:

- Dignified Trade, with suppliers;

- Dignified Engagement, with commnities, of place, and of interest;

- Dignified Reckoning with the consequences, on Nature, on Society and on our shared Future;

- Dignified Working, in the workplace;

- Dignified Dealing, in the marketplace, wth both consumers and competitors; and

- Dignified Sharing with the savers whose savings are the “raw material” out of which capital is formed through financing.

When our common sense is that the capacity of Pensions & Endowments includes and is limited by the mathematics of allocation through Exit by Sale to extract profits from selling price, there is not much for us to deliberate about, regarding their exercise of that capacity.

“the [securities trading markets professionals] have pushed out the attorneys [as champions of the common sense of sensible people who take the time to make the effort to make ourselves familiar with such matters] from interpreting fiduiary duty”

– Keith Johnson

But if we update and upgrade our common sense, to see that Pensions & Endowments also have the capacity, under the circumstnaces now prevailing, to allocate their aggregations through the innovative, new financial mathematics of Exit through Amortization, to a ”forever” cost of money, from “forever” businesses, we will also see that there is much we can and should be deliberating about, regarding where this money can and should be made to go to curate the businesses that curate the technoloiges that curate the choices the curate the economy that curates society that curates the future as our true frontier.

What future do you want our Pensions & Endowments to be financing for you?

Join the journey,![]() by talking about the crises,

by talking about the crises,

their origins and their resolutions.

Next: Why Me?