rebooting the system, to reset the code, and purge the corruption

The logic of Money for Finance has become corrupted by Capital Markets capture of Social Trust Funds, through the false assertion that more for them will always also mean better for us.

We need to purge this falseness from our sociologies of social choosing using money, through innovations in fiduciary finance, and the innovation of Fiduciary Activism as new 21st Century planetary citizens in the new 21st Century planetary commons of Equity Paybacks of Fiduciary Money for INCOME with IMPACT, to reset the code of Money for Finance as how society controls the flow to inform our future, and our present.

“a technology that communities use to trade debts”

- Micheal Mainelli

a legal instrument for effecting transactions between people who are separated by distances of time, place and social connection (“you don’t have to trust the person, if you can trust their money”)

the social energy for directing our individual insights and initiative towards some activities (where money can be made) and away from others (where there is no money to be made)

There are few words in the English language that so completely express the roiling tumult of conflict and contentiousness that is our human way of being in the world as this one word, “money”.

By design, money is inert. A simple measure that in itself says nothing about the value of what is being measured. A purely factual recording of a quantity.

But what is being measured, what is being quantified by money, is our human relationships with each other; our worth, as a human, to another human. And that is very dangerous territory, this territory of our worth to others. It is a symphony of rationality and and a cacophony emotion, of thinking and feeling, of thoughtfulness and thoughtlessness, every single note of which is sounded in some way through money.

Money does not exist in Nature. It is completely made up, a purely human invention. A thing that is no thing. Nothing.

And yet it is the most powerful thing in the whole of human experience. The root of all evil. And the best revenge.

We all use money.

Some of us want it.

Some wish we did not have it.

We all need it.

Few really understand it.

Because our stories about money are as confused and conflicted as the relationships that we energize through money.

To have money is to have power over others. To be without money is to be without power, forced to become indentured to others, or driven to rely on our wiles in an effort to beguile.

To be sure, there is an empirical residue of human emotion that manifests without money: the care and caring of mother for child, of family and friends; the animosities of rivals and hatred of enemies.

But mostly, people live together using money.

Given the importance of money to our human way of being together in society, it seems we should have a universally accepted and clinically precise language and vocabulary for talking about money, much the way we have a language for talking about language. We know what words are and how they are used. When they are being used correctly, and when they are being corrupted.

But we don’t know so much about money.

Why not?

We are taught to believe, through the Great Markets vs. Government Regulation Debate, that money does not matter, that all social choices are made either freely, in the markets, or coercively, through politics.

Price v. Policy

Private v. Public

Individual v. Collective

Freedom v. Coercion

This story is always a little bit skewed.

Markets are always presented as a perfectly virtuous expression of our collective wisdom as the sum total of individual choices freely made by each of us, individually, each individually choosing according to our own personal and individual moral compass, in which no individual is ever forced to make a choice they do not freely choose to make.

Government, on the other hand, is always presented as vaguely sinister (even though it is a constitutional representative expression of our free choices, as voters at the ballot box, through electoral politics), an oppressive force that imposes a collective will as a constraint on personal freedom. The reasons why force is sometimes used in society to constrain freedom are never really explored, or even acknowledged as being worthy, not to mention necessary, to maintain social cohesion and a dignified quality of life.

This narrative does not allow space for exploring the function of government in righting the wrongs that sometimes occur in the markets, when bad actors act badly, and when institutions become corrupted in their exercise of authority untrue to their agency and purpose.

We need to teach ourselves to see this story as the special pleading for the special interests of those who control money in society today, who sell/tell this story to keep us from seeing the importance of money, and the illegitimacy of their control over money.

We need to teach ourselves to see the truth that people make choices in the markets by paying a price, and that prices are paid using money, so that those who control the money determine who can pay the price, and therefor who gets to make what choices.

If we want individuals to be free to make our own choices, for ourselves, then we need to institutions for controlling the flow of money that reliably flow money to individuals, fairly and equitably, and not concentrate control over the flow of money in the hands of a few, who use it to oppress the many.

The truth about markets that we are never allowed to acknowledge according to the prevailing story of our time is that money matters in the markets: if you have the money you can pay the price, which means you get to make the choice; if you do not have the money, you cannot make the choice. Instead, choices that affect you, personally and individually, will be made for you by others, without your consent, or participation: because they have the money, and you do not.

The much ballyhooed perfect freedom of the markets today is, in fact, a most imperfect unfairness, and oppression of those who do not have by those who do.

Because the markets are not shaped by people.

They are shaped by money.

Or, rather, they are shaped by people spending money to pay the price of making a choice.

Our freedom to choose is contained in our control over money.

If we control a lot of money, we have much freedom.

If we do not control much money, we do not have much freedom.

And when a few control a lot of money, and many do not control much money, the markets become arenas of oppression by those who have, lording it over those who do not.

This dominance of the few over the many is then justified with the trite assertion that we each are responsible for how much money we control: if we control a lot of money, that is a consequence of our superior merit, and personal morality; if we do not control much money, that also is a reflection of our own personal merit and morals.

This assertion is false on its face, and needs to be rejected utterly.

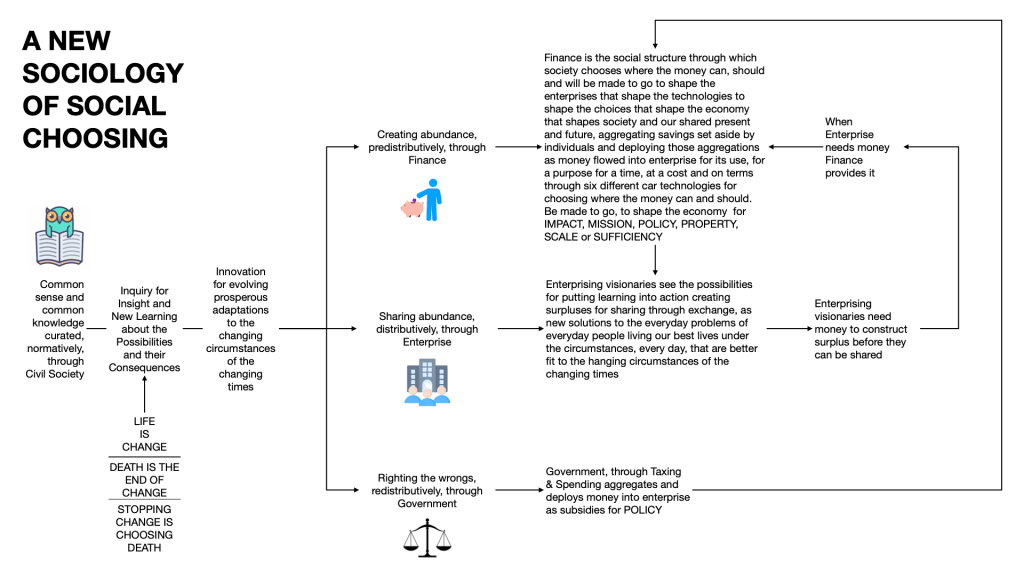

Money is a sociology of social choosing that is controlled by institutions of agency, authority and accountability that are created by design to operate according to legally specified codes of instruction for authenticity and integrity in their institutional exercises of their institutional authority/power true to their institutional agency/purpose/mission.

If the code gets corrupted, institutional authority gets exercised deviantly from institutional agency, spreading discord through society that manifests as the oppression of the many by the few.

Today, the code of money has become severely corrupted, and discord is spreading like an infection, around the planet.

We need to reboot the system of institutions that control the flow of money, to reset the code, and purge the corruption, before we can restore cohesion to society, and health to our partnership with the planet.

The first step in rebooting the system is taking an inventory of its parts, to discover what is there, that the story we are being sold/told is hiding from us.

Then, we have to look at how those parts are designed to work, correctly, so that we can then diagnose where and how they are currently working incorrectly.

Only then can we hit the reset button.

Let’s begin with an inventory of parts.

When we look at money we see a difference between the physicality of the thing we call money, and its functioning in society.

When money is made to flow through institutions of finance, it becomes infused with a logic and a language for talking about:

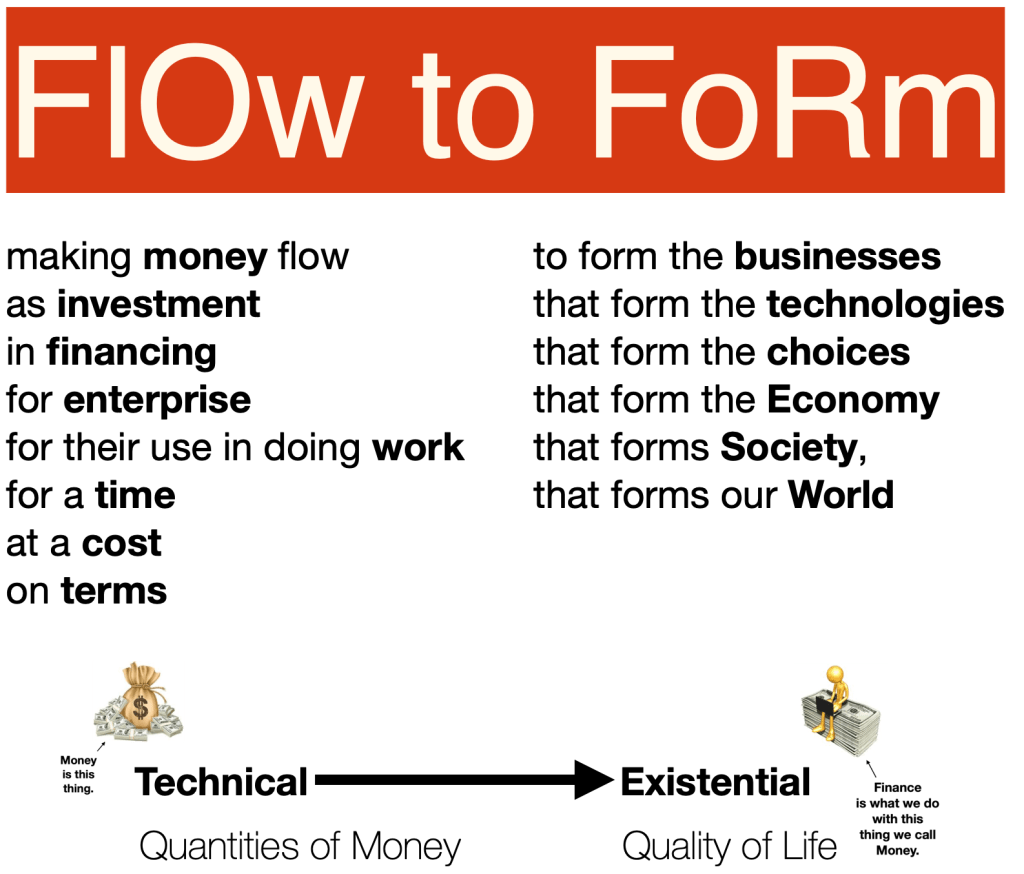

- how money set aside by others, for a purpose, for a time, as savings for investment in financing for enterprise gets aggregated, and

- how those aggregations get allocated as money made to flow into enterprise for its use in paying its cost in order to realize its price, for at time, at a cost, and on terms that inform how that business does business expressing its technology as choices made available to others to inform the economy that informs society that informs our future.

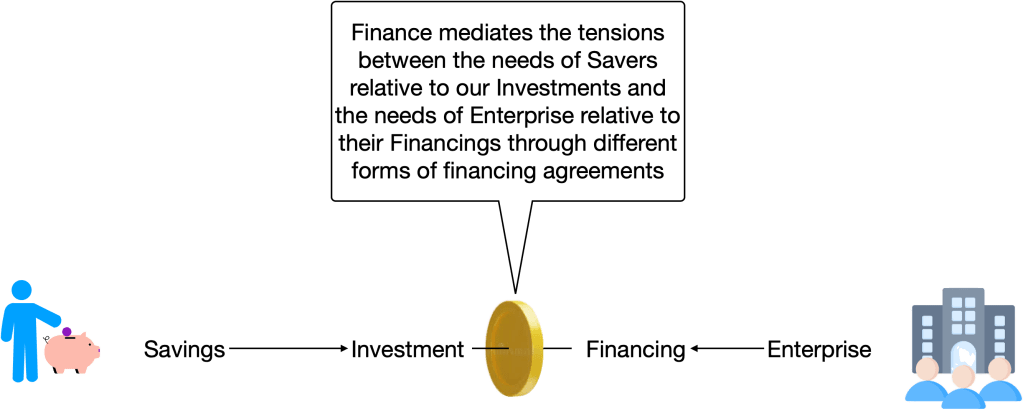

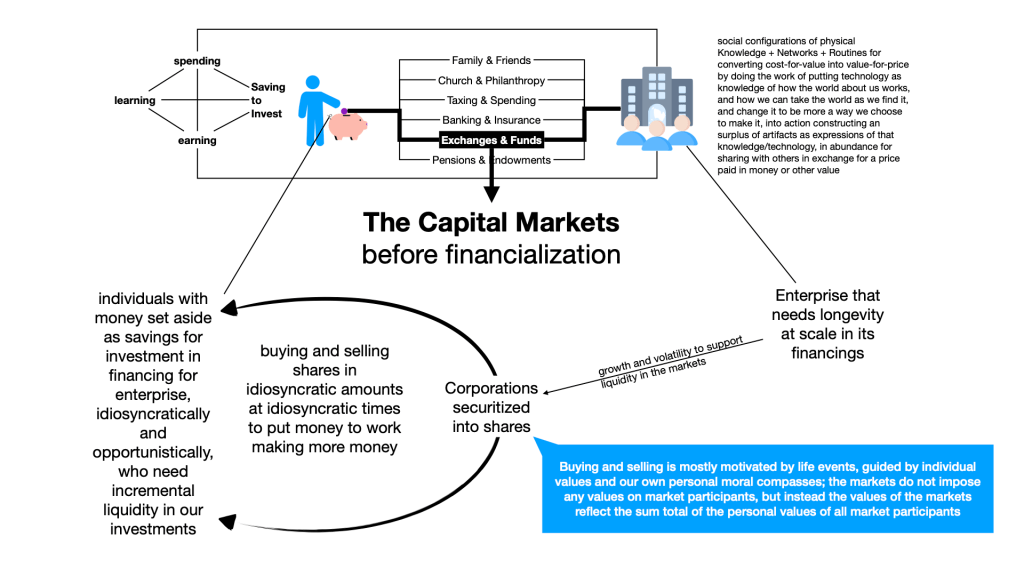

This gives us a new way of talking about the function of finance, generically, as the aggregation and allocation of money set aside as savings for investment in financing for enterprise.

This shows us that investment and financing are two words that reference the same transaction from two different points of interests – the obverse and the reverse of the same coin, if you will – where investment is the transaction viewed by the saver, and financing is that very same transaction viewed by the enterprise.

This framing lets us see that the function of finance is to mediate the tensions between our needs, as Savers, relative to our Investments and the needs of Enterprise relative to its Financings.

This invites reflection on how it is that we, as individuals, use money to shape our own personal and private worlds in which we each live our own best lives, as best we can, under the circumstances then prevailing, out of the public world of social choices that we all make together, through enterprise for the exchange of an abundance of technologies, out of the world of Nature into which we each and all are born

This reflection shows us that we each use money to:

- learn about how the world about us, both the natural world and our human worlds, work, and how we can take those worlds about us as we find them, and change them to work more a way we choose to make them, through technology as practical knowledge of the world and how it works in various specific way;

- earn money through participation in enterprise, where “earn” is used as broadly as possible to encompass any activity that results in our gaining control over money (even if that activity involves nothing more than being born to parents who have control over money and who pass that control to us, through laws of inheritance – a topic much to be explored in the use case of wealth inequality and its impact of social cohesion)

- spend money to pay the price to acquire surplus of technology from enteprise, that we desire to use in shaping our own personal and private worlds in which our world works more the way we choose to make it;

- save money we earn but do not spend, to spend later; and

- invest our savings for diverse purposes, that include:

- caring for our own;

- caring for others;

- contributing to the public fisc for paying the costs of public health, public safety and social cohesion through shared wellbeing;

- safekeeping (physically and accounting for credits and debits) and future transacting;

- idiosyncratically and opportunistically putting money to work making more money; and

- programmatically providing certainty against certain of life’s future financial uncertainties.

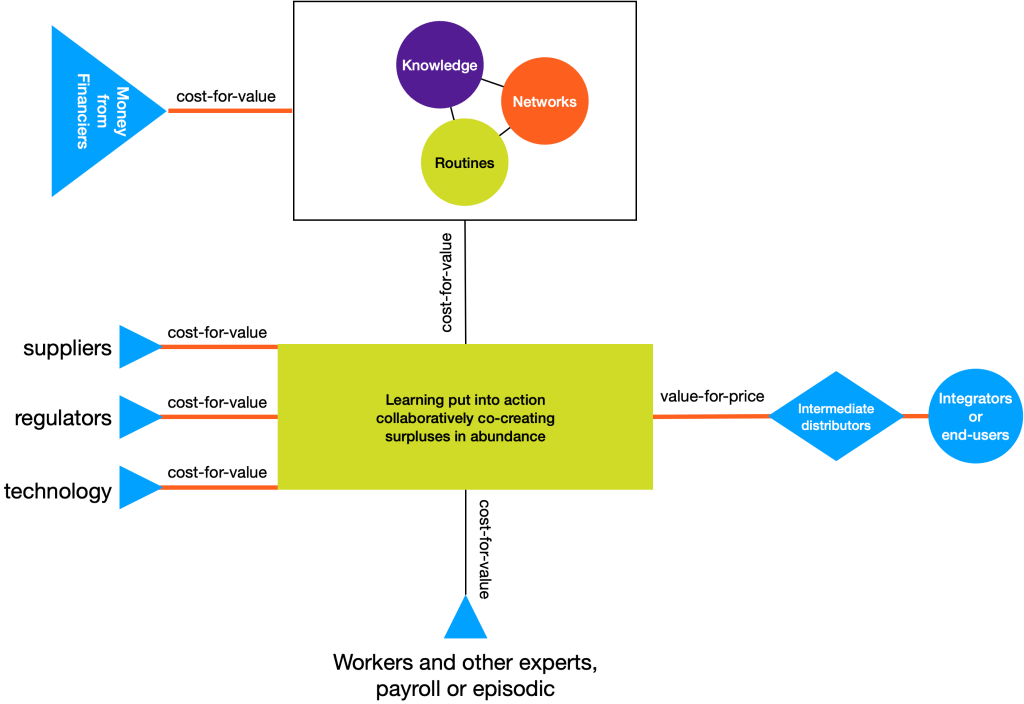

This also invites reflection on Enterprise, looking beyond the prevailing popular legal form of the corporation, to see the physicality of how it is that business actually does business.

Physically, an enterprise can be seen as:

- a social configuration of Knowledge + Networks + Routines

- for converting cost-for-value into value-for-price

- by doing the work of constructing a surplus of expressions of technology,

- as practical knowledge of how the world about us works in some specific way, put into action changing the way that world works, in that specific way, to make it work more a way we choose to make it, in some specific way

- in abundance for sharing with others

- in exchange for a price paid in money or other value.

This way of seeing Enterprise as a social configuration for doing physical work lets us see how it is that Enterprise needs money to pay its costs before it can realize its price.

When Enterprise needs money, Finance provides it.

This let’s us see Finance as an institution of agency, authority and accountability for aggregating money set aside by others, as savings for investment in financing for enterprise, and allocating those aggregations as money made to flow into Enterprise for its use in paying its costs in order to realize it price, for a time, at a cost and on terms that inform how the business does business of expressing its technology as choices for others that informs the economy that informs society that informs our future.

This is a most important function in society, that must be done correctly, if the people are to live well together, and apart.

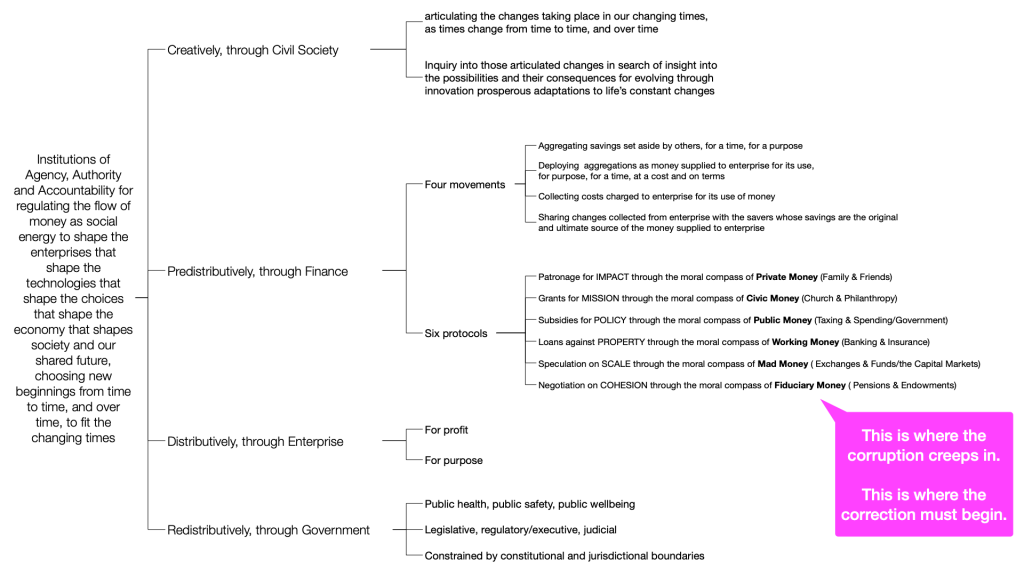

Understanding how Finance functions correctly begins by considering the different reasons that people set money aside as savings for investment in financing for enterprise, and matching reasons with a logic of financing that fits.

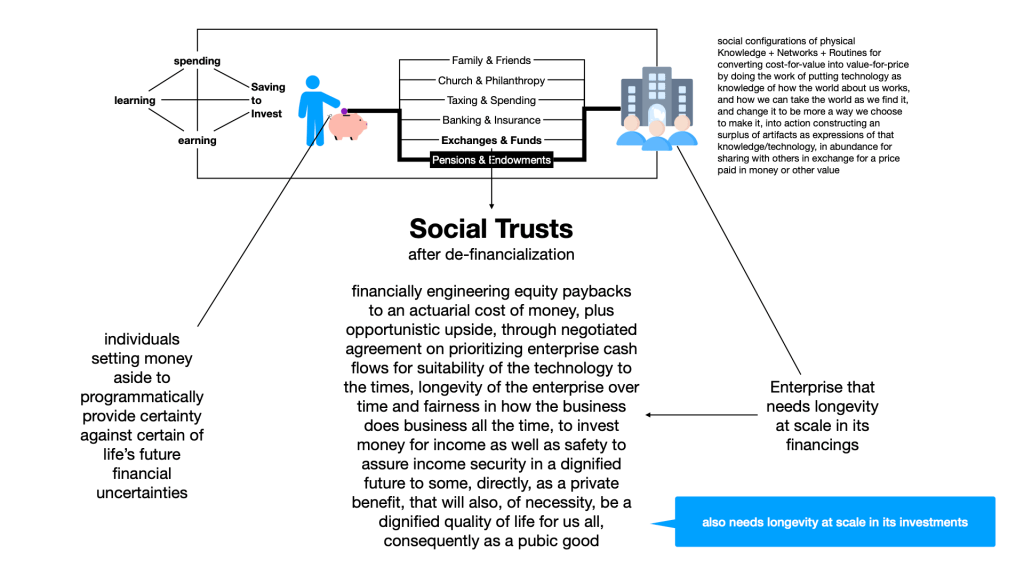

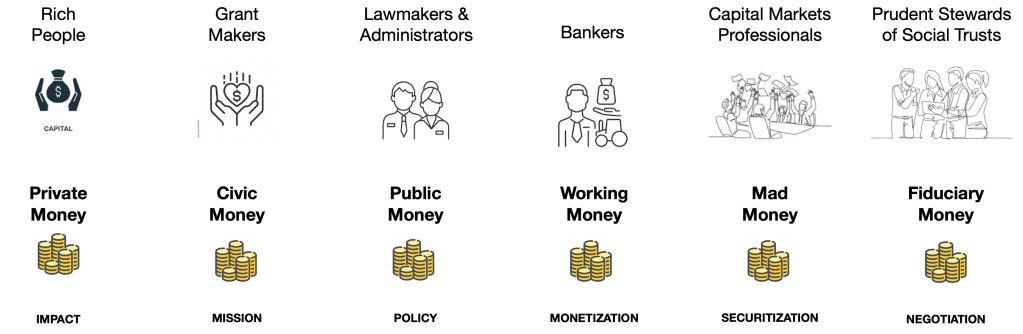

This gives us our inventory of six different kinds of savings matched to six different logical forms of finance:

- Private Money set aside to provide for our own, aggregated through Family & Friends and allocated as patronage for IMPACT (where Impact is whatever the family and its friends choose as good for the family, and its friends);

- Civic Money set aside to provide for others, aggregated through Church & Philanthropy and allocated as grants for MISSION;

- Public Money contributed to the public fisc, for public health, public safety and social cohesion, aggregate through Taxing & Spending, and allocated as subsidies for POLICY;

- Working Money set aside for safekeeping and future transacting, aggregated through Banking & Insurance, and allocated through monetization of PROPERTY;

- Mad Money, set aside to put money to work making more money, opportunistically and idiosyncratically, aggregated through Exchanges & Funds and allocated through securitization for speculation on SCALE; and

- Fiduciary Money set aside to programmatically provide certainty against certain on life’s future financial uncertainties, aggregated through Pensions & Endowments, and allocated through negotiation for SUFFICIENCY.

This way of seeing Finance also gives us a more complete way of understanding how we, as individuals, contribute to, and form a critical component of the economy, as learners, earners, spenders, savers and investors to make our own personal and private world in which we each live, personally and private, out of the shared, public world that we make together, through enterprise for the exchange of technologies, out of the world of Nature into which we each and all are born.

This allows us to articulate a more expansive sociology of social choosing than the confusing-because-incomplete Great Markets v Government Regulation Debate, brought to us by Neoliberalism, that includes both Civil Society and Finance as institutions of agency, authority and accountability, alongside Enterprise and Politics, within a new social narrative of being human in society, through economy, using money on a planetary scale in the 21st Century and beyond, in an artificial world of technology solutions that we make for ourselves in which to live, out of the world of Nature into which we each and all are born as

- a mutual aid society for sharing an abundance of technology solutions to the everyday problems of everyday people living our own best lives as best we can under the circumstances then prevailing, every day

- through networks of enterprise and exchange

- using money as a legal instrument for effecting transactions between people who are separated by distances of time, place and social connection, that is also the social energy that directs our individual insights and initiative towards some activities, and away from others

- to construct, and episodically de-construct to reconstruct, a safe and dignified house for humanity

- within built environments of Urban, Rural, Curated and Left-Alone environments

- along the creative edge of a constantly changing and adaptively evolving Human partnership with Nature, and each other,

- choosing new beginnings from time to time, to better fit the changing circumstances of the chaining times

- through inquiry for insight and new learning that can inform innovation

- making new choices more popular as better fit to the circumstances then prevailing

- while letting previously popular choices fade into history as a good fit to the circumstances prevailing at an earlier time

- driving the flourish and fade of the social contract between enterprise and popular choice

- that is the true pulse-beat of our prosperity, and the real story of our human history

- normatively, through Civil Society

- predistributively, through Finance

- distributively, through Enterprise, snd

- redistributively, through Politics, Policy, Law and Government

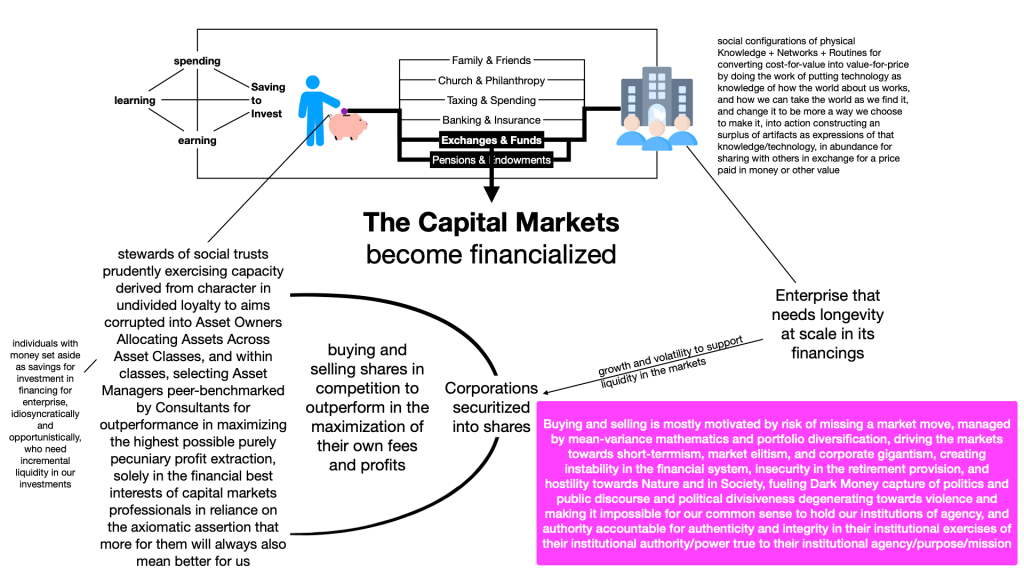

This lets us see the source of the corruption, because Fiduciary Money is not being true to its own purposes, but is instead allowing the Capital Markets to take control.

Without fiduciary money, the capital markets operate authentically, mediating the tensions between us, as individuals, who need liquidity in increments in our investments, and enterprise that needs longevity at scale in their financings, by negotiating large scale, long dated financing agreements with Enterprise, and securitizing those agreements into large numbers of smaller, legally equal, commodity shares of ownership that can be bought and sold at market clearing prices between market participants in the markets for maintaining market clearing prices for such shares, through volatility and growth in market clearing prices, without involving the Enterprise in those purchases or sales (but requiring Enterprise to support volatility and growth in the market clearing price for its share through a social contract it enters into with the markets for maintaining market clearing prices on such shares).

When the Capital Markets took control of Fiduciary Money, beginning in the early 1970s, they became financialized, as participation in the markets came to be dominated by capital markets professionals trading professionally with fiduciary money that had no reason to sell the shares they bought except to extract profits opportunistically. These market professionals competed for Assets Under Management, and the fees and profits they can extract from Assets Under Management, by outperforming each other in maximizing the highest possible purely pecuniary profit extraction, through price taking in the public capital markets, relying on mean-variance mathematics to model diversified portfolios to mimic the movement of the markets, overall, and over time, or through financially engineering “value creation” for profit extraction in the private, alternative capital markets.

This sales boast by Asset Managers competing for Assets Under Management (and the fees and profits they can extract from Assets Under Management) replaced our common sense, as people familiar with such matter, of prudence in the exercise of capacity derived from character, under the circumstances then prevailing, in undivided loyalty to their aims, as specified in the private and public laws of their creation, corrupting the code of common sense, which corrupted the code of social trust practice, which corrupted the code of the capital markets which is corrupting the code of the corporation which is corrupting the code of enterprise which is corrupting the code of the economy which is corrupting the code of society which is corrupting our future possibilities for living cohesively and with dignity.

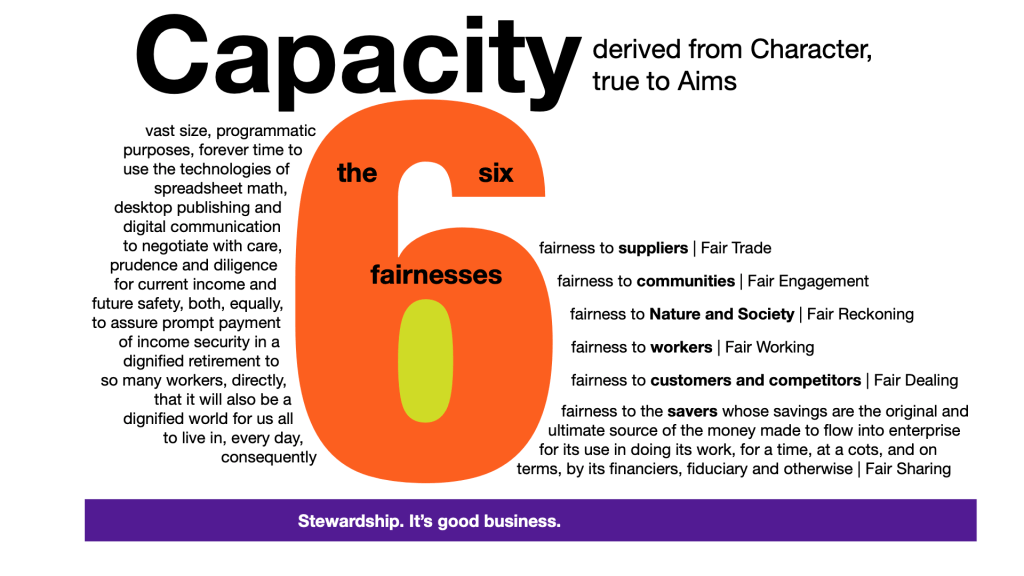

The way to purge this corruption is to go back to the text of the law of fiduciary duty as it applies to social trusts, and reassess the capacity these trusts derive, under the circumstances now prevailing, from their capacity of vast size, programmatic purpose and forever time, to use the person computing technologies of spreadsheet math, desktop publishing and digital communication to financially engineer (see Private Equity) equity paybacks (see Real Estate Equity) to an actuarial/fiduciary cost of money, plus opportunistic upside, from actuarial cash flows prioritized by contract for:

- suitability of the technology to the circumstances then prevailing

- longing of the social contract between the enterprise and popular choice and

- fairness in how the business does business across all six vectors of fairness in how business does business:

- fairness to suppliers (Fair Trade);

- fairness to communities, of place and of interest (Fair Engagement);

- fairness to Nature and Society snd the Future (Fair Reckoning);

- fairness to workers, and in the workplace (Fair Working);

- fairness to customers and competitors (Fair Dealing); and

- fairness to the savers whose savings are the original and ultimate source of the money made to flow into enterprise as financing by it financiers (Fair Sharing).