Mindsets map out the possibilities, for choices that can be made, and the consequences if we make them.

In social activism, mindsets are like frames that show us the problem, and its solution.

If we don’t adopt the right mindset, we won’t view the problem through the right frame, and won’t be able to see the right solution.

We get trapped in actions that lead to inaction.

We can see this, especially, in planetary scale problems, like climate.

Whether we choose to accept this or not, all social activism today views the possibilities through a Neoliberal mindset of the Great Markets vs, Government Regulation Debate that lets us see only two strategies for individual participation in social action: boycotts or protests.

Carbon footprints are a boycott.

Divestment is a boycott.

Carbon offsets are a protest, demanding that a price be placed on carbon, voluntarily, to avoid government regulation, or through government regulation (presumably on the theory that if we price carbon properly into the cost of energy extracted from hydrocarbons then the markets will become a vehicle for “transitioning away from fossil fuels in a just, orderly and equitable manner”, as COP28 correctly concluded that the must, although the exact mechanism by which transition is going to happen is never made very clear – it seems to be a case of blind faith “that here a miracle occurs”.

Shareholder activism/engagement is a protest.

Sustainability, ESG and DEI, all call for disclosure to inform either boycotts (divestment) or protest (engagement).

None of these actions are having any real impact, because they are not focused on fixing the problem, which is financialization.

It’s a small problem hidden inside a lot of context that needs to be de-constructed, which makes it rather a formidable challenge of language and words.

Here’s the assessment.

The financialization of our common sense of the capacity that social trusts derive from their legally constituted capacity of vast size, programmatic purpose and forever time by our willing and complicit acclimation to of the special pleading for the special interests of capital markets professionals in exercising monopoly control over the tens of trillions of society’s shared savings aggregated into these social trusts for the public good for their own private benefit has allowed the transformation of Prudent Stewards of Social Trusts into Asset Owners Allocating Assets Across Asset Classes and within classes, selecting Asset Managers peer-benchmarked for outperformance in maximizing the highest possible purely pecuniary profit extraction from the capital markets, solely in the financial best interests of capital markets professionals in reliance on the axiomatic (and fundamentally false) assertion that more fees and profits for them will always also mean a better quality of life for us.

And Hey! Presto!, as our common sense gets replaced by their expert knowledge the aim of these social trust shifts from investing money for income as well as safety to assure income security in a dignified gut to outperforming the maximization of the highest possible purely pecuniary profit extraction from the capital markets.

Except it doesn’t.

The law has not changed. Only our common understanding of what the law requires and allows has changed.

We can correct our common understanding if fiduciary duty for social trusts, and rectify our common sense of their agency and authority, in order to reassert accountability to us, by going back to the text of the law, to see that fiduciary duty is a constraint on discretion that requires prudence as a process, and loyalty to the instructions in the documents, as an absolute.

The standard is not outperformance, but the faithful performance of the social purpose for which those social trusts are given social license to be and to continue by us, as citizens, and tax-exemption subsidies paid for by us, as taxpayers.

That purpose is not to maximize anything.

These social trusts are not owners of anything. They are stewards of money entrusted to their discretion, within the constraints of prudent process and absolute loyalty to purpose, which is:

- to invest money

- for income as well as safety

- sufficient to their own longevity

- able to make the contractually calculated payment to contractually qualified recipients at contractually specified intervals, across the generations

- to assure

- income security in a dignified future for some, directly, as a private benefit, for us all, consequently, as a public good.

The pathway of return to common sense lies through a technical answer to this technical question:

What capacity do social trusts for Pensions & Endowments derive from their legally constituted character of vast size, programmatic purpose and forever time, under the circumstances now prevailing?

One clue to the answer can be found in the now-common practice of Private Equity raising financing from Pensions & Endowments and using that financing to financially engineer financing agreements based on equity as ownership for extraction, negotiated directly with enterprise of any size, in any business, anywhere on the planet.

That practice shows us that social trusts for Pensions & Endowments have the capacity to use the circa 1983 personal computing technologies of spreadsheet math, desktop publishing and digital communication to financially engineer financing agreements with enterprise, directly.

Another clue can be found in the long-standard practice in Real Estate of raising financing, more from Insurance than from Pensions & Endowments, but still from institutions with a purpose to the future, and using the financing to financially engineer equity paybacks to an agreed cost of money, plus opportunistic upside, from real estate development projects prioritized by contract to align with the institutional values of the institutions providing that financing.

If we combine Private Equity + Real Estate in our imaginations, we can clearly see the capacity that Pensions & Endowments derive from their capacity of size, purpose and time, to financially engineer equity paybacks to an actuarial/fiduciary cost of money, plus opportunistic upside, from enterprise cash flows prioritized by contract for:

- suitability of the technology to the circumstances then prevailing

- longevity of the social contract between that enterprise and popular choice; and

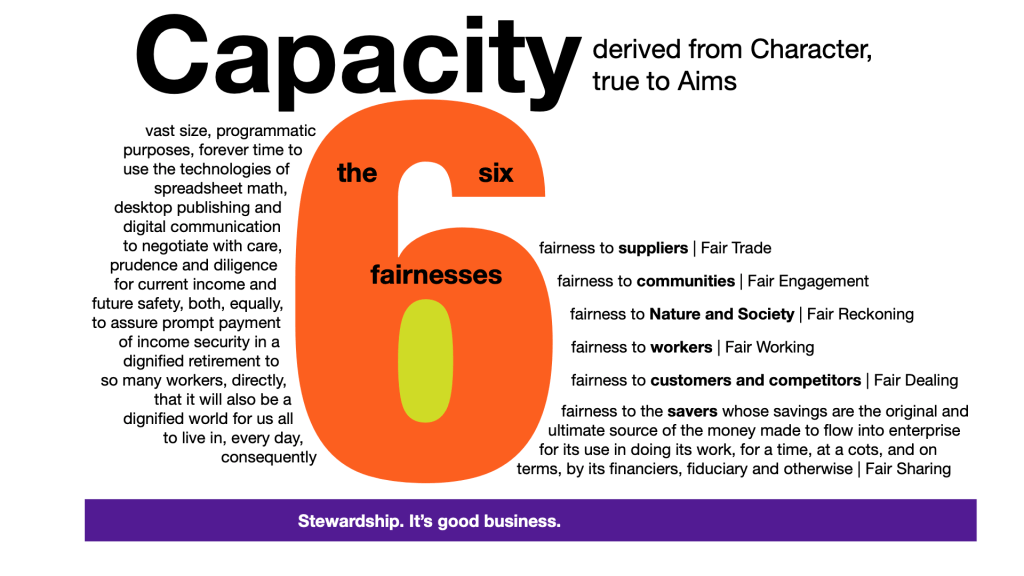

- fairness in how the business does business, along al six vectors of fairness in business:

- fairness to suppliers (Fair Trade);

- fairness to communities, of place and of interest (Fair Engagement);

- fairness to Nature and Society and the Future (Fair Reckoning);

- fairness to workers, and in the workplace (Fair Working);

- fairness to customers and competitors (Fair Dealing); and

- fairness to the savers (that is, to you and me, and all of us) whose savings are the original and ultimate source of the money made to flow into that enterprise by its financiers (Fair Sharing).

If they have this capacity, is it prudent for them to choose not to use it?

What do you think?