Care is mostly about prudence in the exercise of capacity.

Caring is more about loyalty to aims.

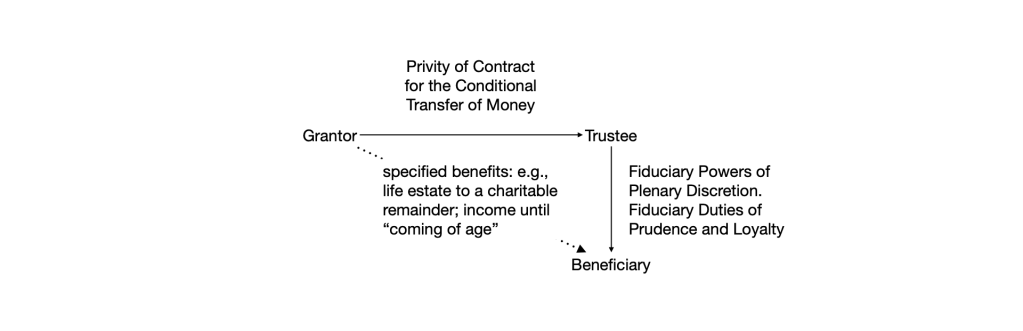

Every trust is constituted for a purpose, and every fiduciary has a duty under law of undivided loyalty to that legally constituted purpose.

Family trusts for private purposes typically provide a life estate to a charitable remainder, to provide for widows until their death, followed by a gift to an alma mater, for example; or to provide income to a minor child (i.e. a child who is too young to manage their own affairs for themselves) until they reach their majority, or other age.

These private trusts for estate planning purposes can only cross two or three generations, benefiting people who are alive, or in utero, at the time the trust becomes effective.

So the fiduciary powers entrusted to the fiduciary steward of a private trust (legally, the trustee) are derived from the capacity of the grantor, and constrained by the size of the trust, who it benefits and how, and the length of time before thet trust is required to dissolve, either by direction, or by law (the Rule Against Perpetuities). Essentially, these trustees exercise the powers of their beneficiares, as their alter egos, but within the constraints of the instructions in the trust.

And their duties are to be faithful to those instructions.

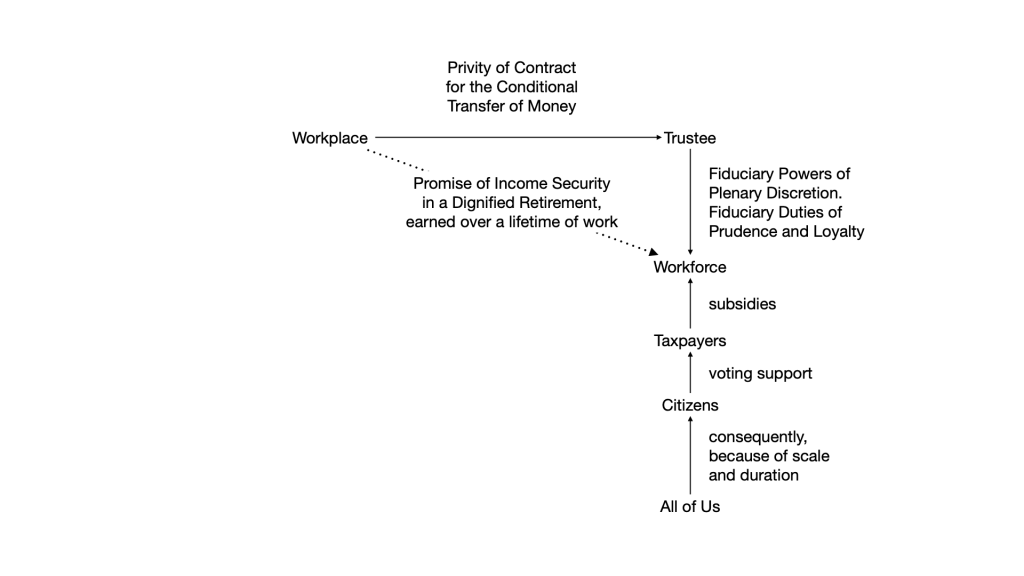

A pension trust is similar, but also different.

It is constituted by a mutual aid society established by a collective bargaining agreement (or equivalent) between a workplace and some or all of its workforce, for averaging the actual costs of making contractually calculated payments to contractually qualified recipients at contractually specified intervals, within statistically significant population of statistically similar individuals.

So a pension trust is social, not private.

It is social, not individual, in scale.

It is social in time, self-perpetuating across the generations, pretty much forever, and not just passing from one generation another, between overlapping generations.

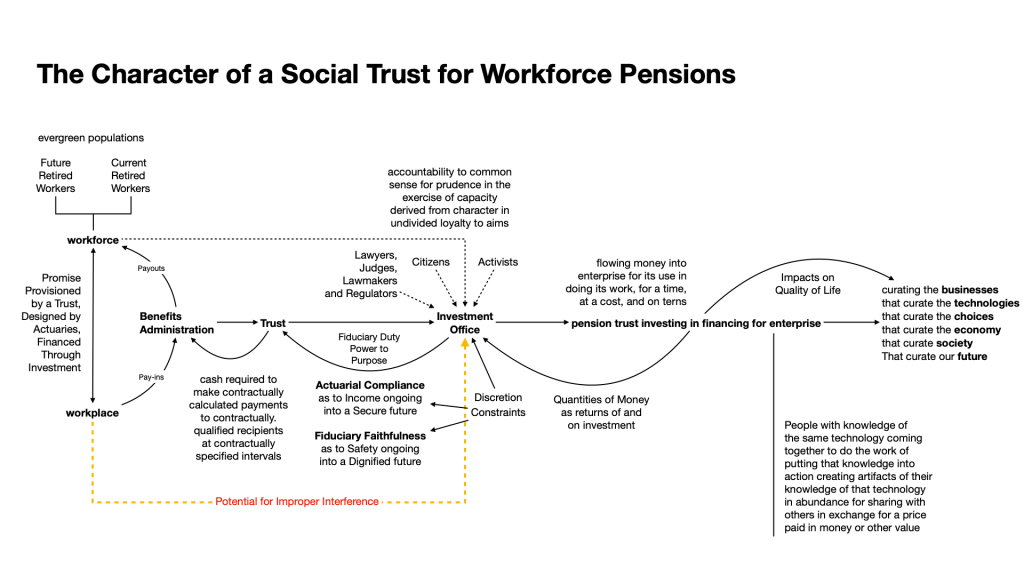

The fiduciary powers of the fiduciary stewards of social trusts for a pension promise by a workplace to a workforce reflect:

- the vast amounts of money entrusted to their plenary discretion (hundreds of millions to billions to tens to hundreds of billions, individually, tens of trillions, collectivley, worldwide);

- their programmatic purpose; and

- their self-perpetuating duration of these “forever machines”.

Since the 1980s, the large, programmatic and self-perpetuating character of the social trust for a workforce pension has given the fiduciary stewards of those trusts, under the circumstances now prevailing, the capacity – the time, the purpose and the time – to use the personal computing technologies of spreadsheet math, desktop publishing and digital communication to allocate the aggregations of money entrusted to their plenary discretion through a new mathematics of exit by amortization to an actuarial/fiduciary cost of money, plus opportunistic upside, from enterprise cash flows prioritized by contract to align the values that get valued in the way the business does business with the fiduciary loyalties of the fiduciary stewards to the assurance of income security in a dignified retirement to so many, directly, as a private benefit, that it is also a dignified future for us all, consequently, as a public good.

The problem is that we have not reconsidered the capacity that a pension trust derives from its character as a large, purposeful and self-perpetuating “forever machine” since the 1970s, BEFORE personal computing technologies became uniquitously available.

So, we took a wrong turning into Exit by Sale in the 1970s, and missed the opportunity to upgrade to Exit by Amortization when that became a possibility in the 1980s.

We can still make that upgrade.

And if we really care, we will.