Capacity is the link between the law ond common practice.

The law specifies the character of a social trust for Pensions & Endowments, and their aims.

Common sense is tasked with adjudicating the capacity that flows from that character, as a matter of fact, under the circumstances prevailing at the time.

The capacity in question of technology, and mathematics.

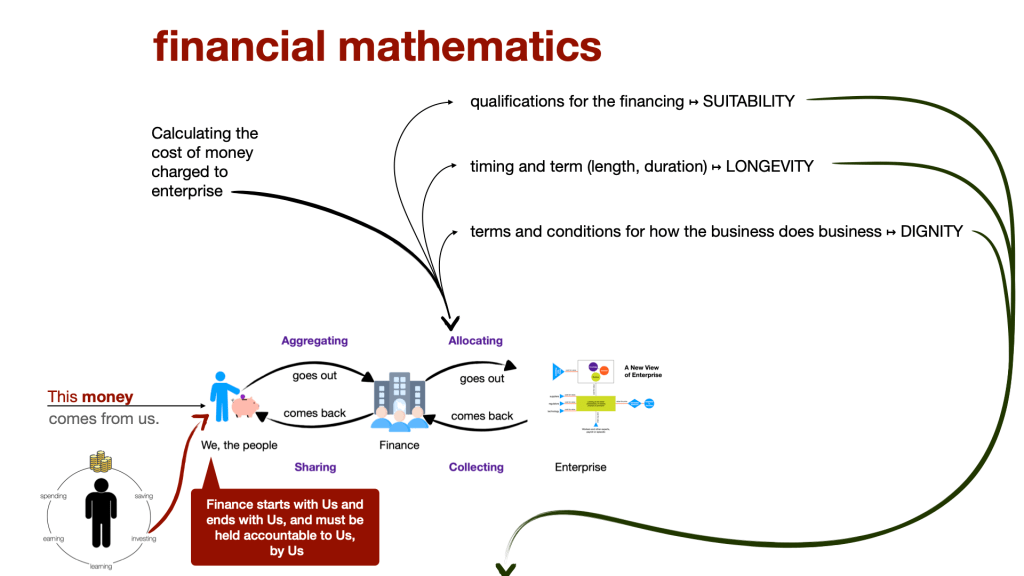

Finance is about money, and money is a number.

Mathematics is the language of numbers.

Finance is also about time.

Time is money.

Money is time.

Money over time is about the capacity to do work, and realize rewards.

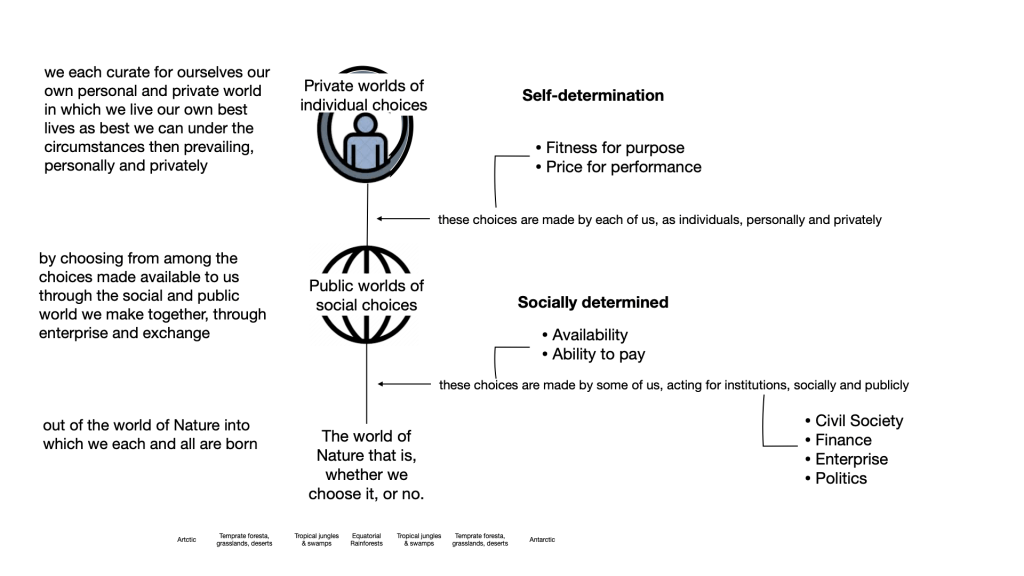

Finance is how society decides who will be allocated the capacity to do what work, in pursuit of what rewards, for how long.

Finance decides those allocations based on future anticipations of the popularity of that work to popular choice: the individual determinations of fitness-for-purpose and price-for-performance by freely self-determining market participants, within the institutionally curated constraints of availability and ability-to-pay.

Finance anticipates future popularity through the mathematics of allocation for calculating the cost to be charged for the use of that money as capacity to do work. This calculation of cost is the lens through which Finance assesses the qualifications of a business for financing, establishes the time and timing of that financing and the conditions that must be honored by the business, in order to retain that capacity through the orginally agreed term, or end date, of the financing.

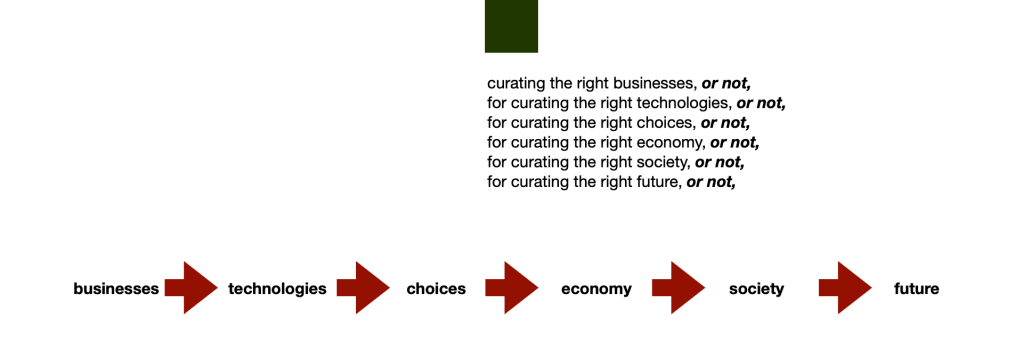

These calculations of cost, qualifications, timing and terms curates which business will be supported in doing business curating the technologies that curate the choices that curate the economy that curates society that curates the future as our true frontier.

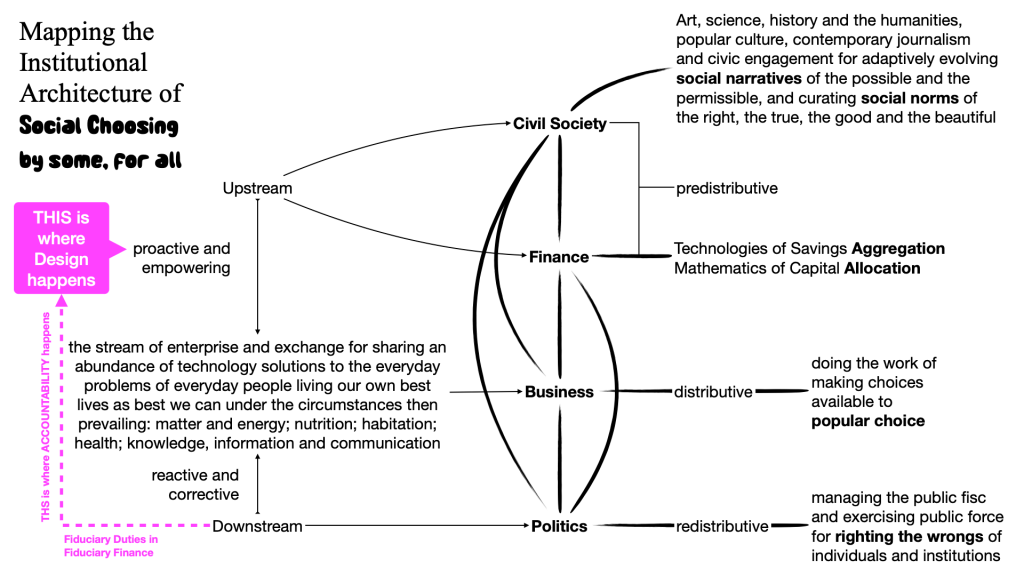

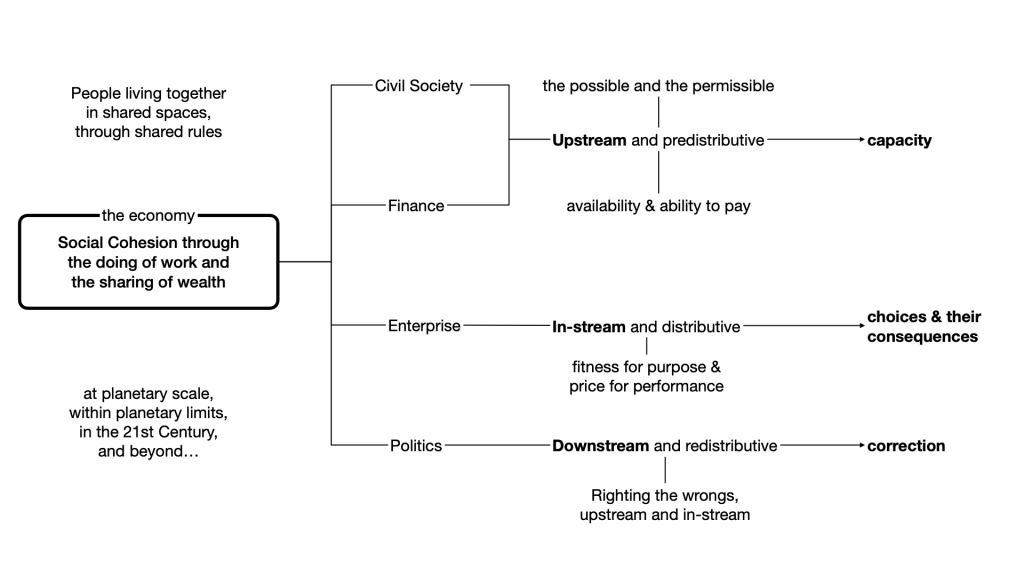

Society does all this curation of capacity, socially, through institutions of Finance, predistributively, and upstream of the stream of commerce, in collaboration with institutions of Civil Society that curate our social narratives of the possible and the permissible, and our social norms of the right and the true and the beautiful and the good.

Business is the stream of commerce, through which choices, and the ability to choose (by having the money that gives you the capacity to pay the price), are distributed within the population and across the generations, through entrprise and exchange.

Politics is the institutions through which society rights the wrongs, redistributively and downstream from the stream of commerce, through policies for managing the public fisc and exercising public force, when Civil Society and Finance, predistriutively, and Business, distributively, get things wrong, when judged against the rubrics of social cohesion.

When we focus in on the institutions of Finance, we see that the agency of these institutions is to:

- aggregate money set aside by others as savings for investment as capital for business, to shift some of the burden of earning from our shoulders to iur wallets; and

- allocate those aggregations to enterprise for doing business through legal agreements on:

- cost

- conditions precedent (qualifications = suitability);

- time and timing (= duration)

- conditions subsequent (terms = how the business does business).

We also see that the authority of these institutions is diverse, reflecting different combinations of technologies of aggregation and corresponding mathematics of allocation, giving us an inventory of differend kinds of Finance that today includes:

- Family & Friends aggregating savings set aside to provide for our own, and allocating those aggregations through the mathematics of patronage for IMPACT;

- Church & Philanthropy aggregating savings set aside to provide for others, and allocating those aggregations through the mathematics of grants for MISSION;

- Taxing & Spending aggregating savings set aside to contribute to the costs of public health, public safety and the public good, and allocating those aggregations through the mathematics of subsides for POLICY;

- Banking & Insurance aggregating savings set aside for safekeeping and future transacting, and allocating those aggregations through the mathematics of monetization of PROPERTY;

- Exchanges & Funds aggregating savings set aside to idiosyncratically put money to work making more money, opportunistically, and allocating those aggregations through the mathematics of profit extraction from GROWTH; and

- Pensions & Endowments aggregating savings set aside to prgrammatically provide certainty against certain of life’s future financial uncertainties, and allocating those aggregations through the mathematics of capacity for AIMS.

This brings us to our question for inquiry in search of insight: what, exactly, is the capacity that Pensions & Endowments have, to allocate their aggregations true to their programmatic aims?

This is a question that humanity really has not considered since the 1970s, when Modern Portfolio Theory for managing pricing risk within diversified portfolios of uncorrelated trading positions in securities traded over the Exchanges, at a time when those Exchanges were populated almost entirely by individuals investing our own savings, for our own account in purusit of our own idiosyncratic purposes, each guided by our own indiviual moral compasses, and each constrained by our own personal moral values, to reproduce at a portfolio level returns that approximate the average of the markets, overall, was the cutting edge of new learing in Finance.

At that time a decision was taken that Pensions & Endowments had the capacity to use Modern Portfolio Theory to allocate their allocations through securities trading, programmatically, and that such programmatic participation in securities trading could be properly prudent and loyal to their aims, and, within the requirements of their fiduciary duties.

Although the law only ever said “could”, a common practice that has become conventional wisdom that works energetically to put itself beyond question, that Pensions & Endowments “must” participate in the securities trading markets; that their fiduciary duties require that they participate, and that they do so as:

- Asset Owners

- allocating Assets

- across Asset Classes

- and within classes, mandating/selecting securities trading markets professionals as Asset Managers

- who are benchmarked against their peers (i.e. other securities trading markets professionals trading securiteis professionally, using forever money sources from fiduciary stewards of Pensions & Endowments)

- by Consultants

- for outpefromance in maximizing the highest possible, purely pecuniary, profit extrction from volatility and growth in market clearing prices for securities trading on market clearing prices in markets for maintaining volatility and growth in market clearing prices for those securities

- solely in the financial best interests of Asset Managers, Consultants, Corporate Executives and other securities trading markets professionals

- on the axiomatic assertion that more money in the securities trading markets (and higher fees and profits for Asset Managers, Consultants, Corporate Executives and other securiteis trading markets professionals and participants) will also always mean a better quality of life for all of us.

Further enforcing the cofusion caused by htis convention, Asset Managers have succeeded in getting themselves identified in common parlance with Asset Owners, as Institional Investors, further obfuscating in our common sense, the differences between:

- the aims of securities trading markets professionsal, to maximise their own fees and profits, and to do all things necessary to perpetuate the conditions under which they can maximize their own fees and profits; and

- the aims of the fiduciary stewards of Pensions & Endowments, to keep themselves ongoing, providing assurance of income security in a dignified future to so many, directly, as a private benefit, that it is also, of necessity, for us all, as a public good, across the generations, and to do all prudent things that are condive to perpetuating conditions of security and dignity, for some, and all, now, and in the future, pretty much forever.

Through the force of this convention, “the attorneys [have been pushed out] from interpreting fiduciary duty” (Keith Johnson), and with the attorneys, the courts, and with the courts, you and me, and our common sense of what capacity Pensions & Endowments actually possess, under the cirumstances now prevailing.

People power pensions.

Shouldn’t people have the power?

– Matt Orsagh, Arketa Institute

This convention has also obscured from our common sense a sense of the upgrade in capacity that became available to Pensions & Endowments in the 1980s, with the invention of personal computing and the information technologies of spreadsheet math, desktop publishing and digital communication.

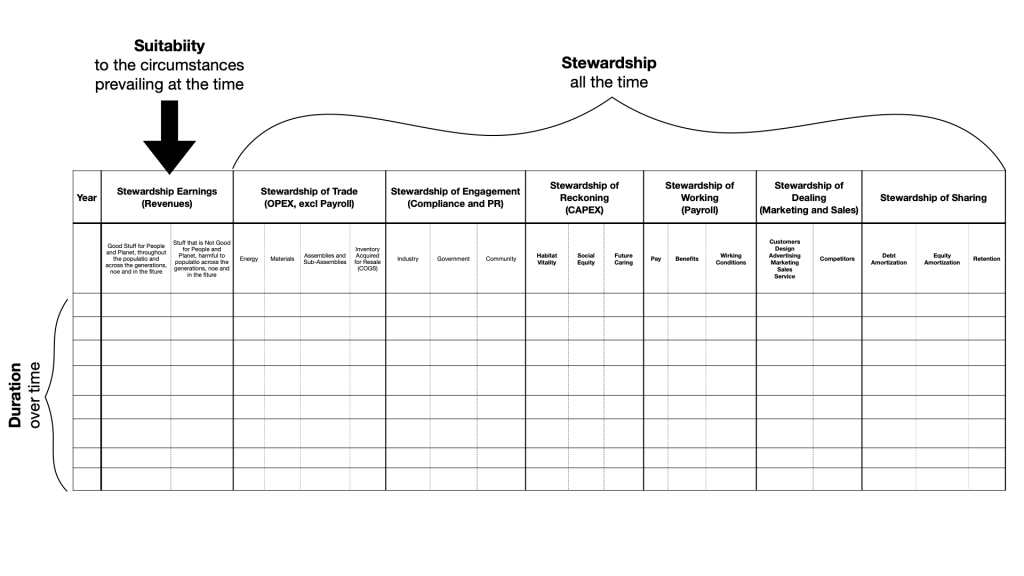

We are not talking, in conversation at the vanguard of public discourse, about the capacity that Pensions & Endowments factually have, under the circumstances now prevailing, to use their size, purpose and time to use these technologies of spreadsheet math, desktop publishing and digital communication to allocate their aggregations through the financial mathematics of Exit by Amortization to an actuarial cost of money, plus opportunistic upside, from enterprise cash flows prioritized by contract for

- Suitability of the technology to the circumstances prevailing at the time;

- Duration of the social contract with popular chocie, over timel and

- Stewardship in how the business does business, all the time, along all six vectors of cash flow through enterprise, including:

- Stewardship of Trade, with suppliers;

- Stewardship of Engagement, with communities, of place, and of interest;

- Stewardship of Reckoning, with the consequences, on Nature, on Society and on our shared Future;

- Stewardship of Working, in the workplace;

- Stewardship of Dealing, with customers, and competitors (pricing policies [Stewardship of Dealing shows up in the Chart of Accounts both as Revenue and as a category of Expense], product desigm [for safety], truth in adverstising, and such);

- Stewardship of Sharing, with the savers whose savings are the rqay material from whcih capital for busienss is formed through Finance.

What? you ask.

Exactly.

We cannot currently make any sense of this capacity in our common sense today.

We do not have the words.

We do not have a story of the possibilities into which we can fit this story.

We need a whole new story, about Money and Savings and Investment and Capital and Business and Financing and Technology and the Economy and Society and the Future as our true Frontier, and Civil Society and Finance and Enterprise and Politics and Nature and Humans and YOU.