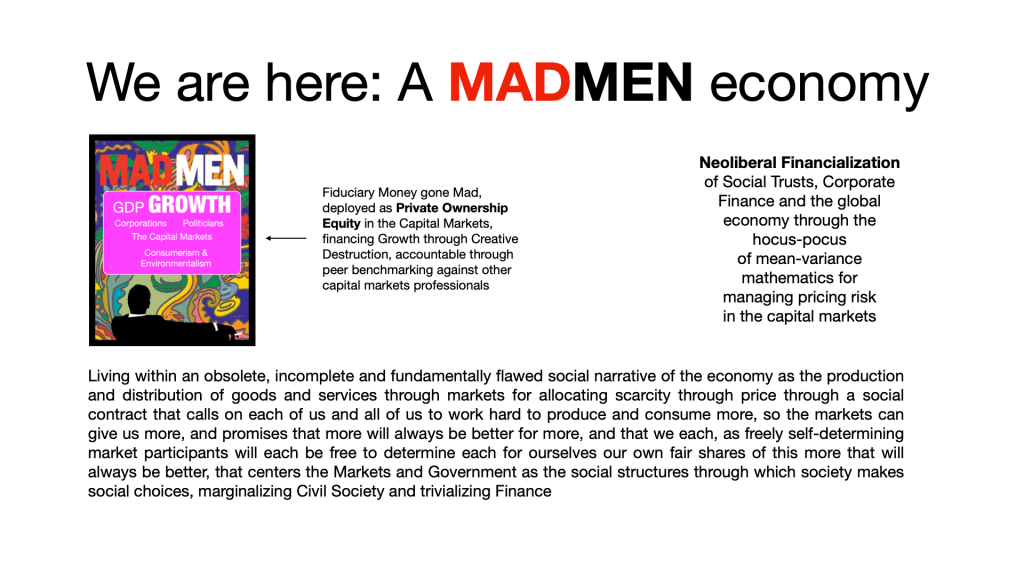

Today we find ourselves schackled to a locked imaginary that Growth is both necessary and sufficient to our making the right chocies for makig the right economy, living within an obsolete, incomplete and fundamentally flawed social narrative of the economy as the production and consumption of goods and services through markets for using price to allocate scarcity in a social contract that calls on each of us andall of us to work hard to produce and consume more, so the markets can give us more, on the promise that more will always be btterm and that we each, as freely self-determining market participants, will each always be free to determin for ourselves our own fair shares of this more that will always be better.

This social narrative centers the Markets and Government, Private and Public, Price and Policy, FREEDOM! and Oppression, as the social structures through which society makes social choices, marginalizing Civil Society and trivializing Finance.

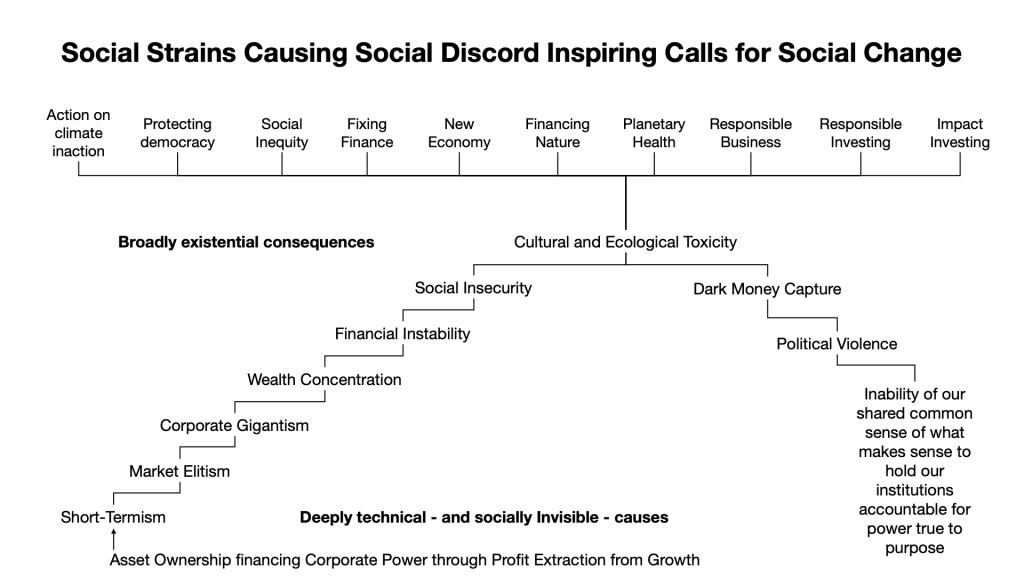

This is a view of the economy seen from the trading pits on the floor of the New York Stock Exchange, through the lens of Finance (which is at once both dispositive and irrelevant) as profit extraction from volatility and growth in market clearing prices for securities in the markets for maintaining volatility and growth in market clearing prices for such securities.

.

It is

- a 19th Century narrative of PROGRESS through technological innovation for economies of scale into an infinitely reeding horizon for endless geobiophysioeconomic expansion within a lived experience that Nature is vast, and we are not, so that we can always just take and take and take from Nature, without ever reckoning with the consequences of our taking, because those consequences would always just disappear into the Frontier, reabsorbed back into Nature, without consequence to us;

- that got reduced over the course of the 20th Century to GROWTH through efficiency as the simple quantitative increase in qualitatively undifferentiated transaction volumes measured in numbers, as prices paid in money, or money equivalents, from one period of measurment to the next.

This is a narrative that derives its power from corporate capture of fiduciary money, as the special pleading for the vested interests of securities trading trading markets professionals in exercising monopoly control over the increasing large quantities of society’s shared savings that are aggregated into social trusts for Workforce Pensions and Civil Society Endowments, that has turned fiduciary stewards of social trusts for social purposes into Asset Owners financing Corporate Power through the financial mathematics of Profit Extraction from Growth in Selling Price.

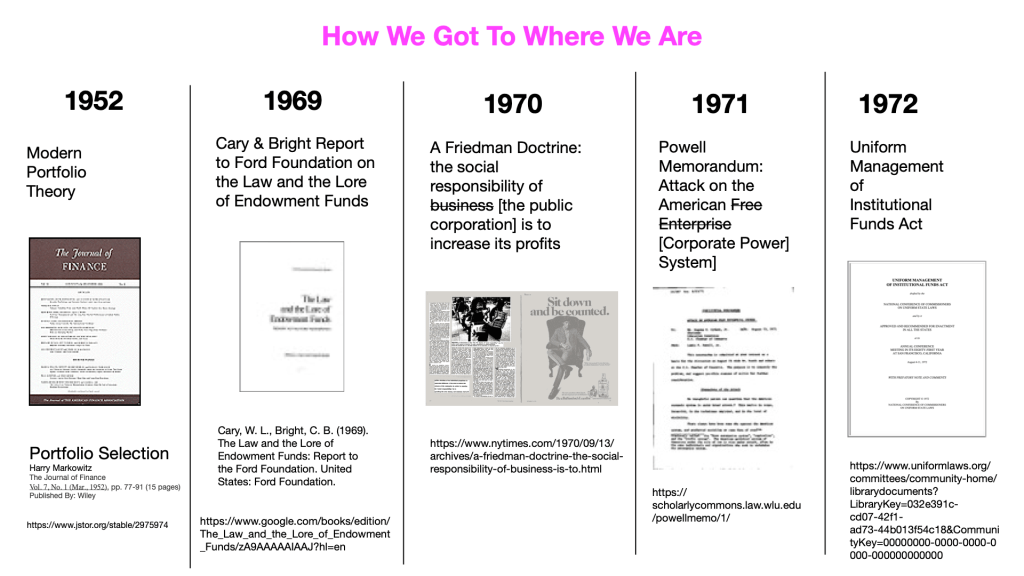

One telling of the story of this capture begins in 1969, with the Cary and Bright Report to Ford Foundation on The Law and the Lore of Endowment Funds.

In this Report, Messrs. Cary and Bright argue that the then-prevailing standard of the Legal List, that effectively limited university endowments and other social truts to allocating their aggregations through the financial mathematics of monetization of property, making loans against a promise to make scheduled repayments, plus accrued interest, to governments and against real estate, placed undue restrictions on the plenary powers of discretionary authority of the fiduciary stewards of these trusts.

Pointing out that the law actually only requires prudence of “the reasonably prudent man (sic) of business”, Cary and Bright argued that then-recent innovations in thinking about price risk management, such as Harry Markowitz’s work on mean-variance, that we now know as Modern Portfolio Theory, may make fiduciary participation in the securities trading markets on a diversified portfolio basis (“may” in the sense of “could”; not in the sense of “does”).

The following year, in 1970, Milton Friedman published his famously self-named “Friedman Doctrine”, that the social responsibility of business is to increase its, by way of an Opinion article in the New York Times newspaper. This was in response to the rising tide of environmentalism and consumer protection that increasingly called on government to make laws regulating the actoins of corporations for the protection of Nature and the consumer.

Friedman’s argument was that Growth as the simple quantitative increase in qualitatively undifferentiated transaction volumes, measured in numbers as prices paid in money, is what Humanity needs, and all that Hu,anity needs, so that if the economy is growing – because busiensses are increasin gtheir profits – then all the problems with externalities, for people, and planet, and people livingon this planet, will be worked out by the markets, through innovation and competiton (and if people are not sharing equally. in this prosperity, well, that is their own fault, for not being industriaous enough, or of high enough moral character).

This, of course, ignores the reality that institutions of Finance determine, predistributively and upstream of the markets, and the stream of commerce, which businesses will qualify for the money they need to be in business, and how those busienss will be required to do business, thereby determining which choices will be made available to popular choice, and which people will have what capacity to choose those choices.

Whar Friedman missed, and what conventional thinking and the dominant narrative still misses, is the difference between:

- the corporation, as a legal form of ownerhip for control of business enterprises that is also a financing agreement between a self-perpetuating hierarchical management bureaucracy and the secufities trading markets (Exchanges & Funds); and

- business as the social organization of physical Knowledge + Networks + Routines for doing the work of transforming cost-for-value into value-for-price.

The corporation as a financing agreement with Exchanges & Funds does have to increase its profits, in order to support growth in the market clearing prices for its corporate shares, which the securities trading markets require as a condition of the financing they supply to corporate enterprise, in order to deliver opportunities to market participants to extract profits from gorwht in maket clearing prices for cporate shares and other securities.

The business as a social reactor for transforming cost-for-value into value-for-price, does not. The social responsibility of business is to honor its social contract with popular chocie, which flourish for a time, before fading in the fulness of time.

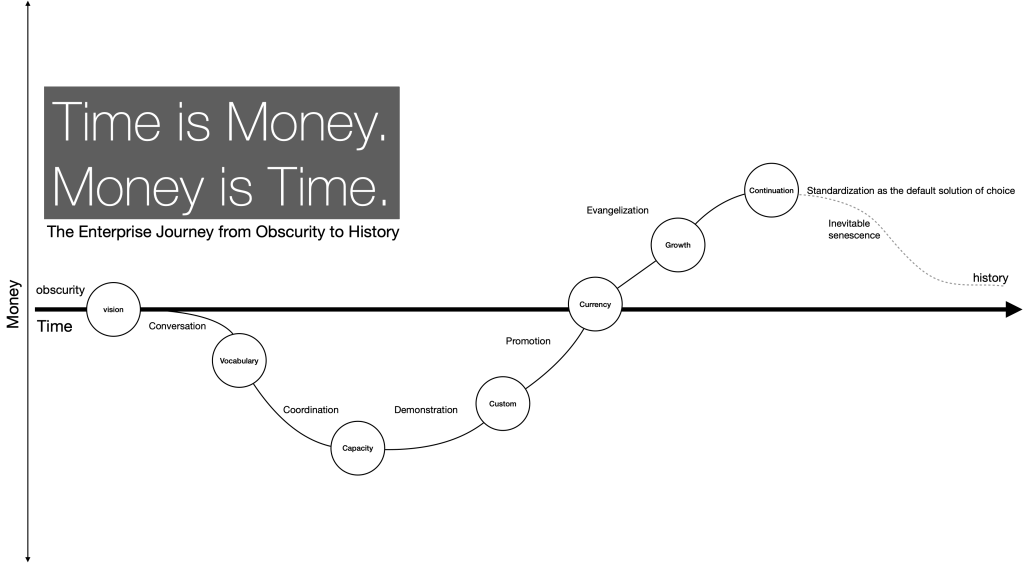

For much of the Enterprise journey, from obscurity into history, the business of business does include increasing its profits. But once the business becomes the default solution of choice within a population, it can be enough for the business to just keep doing its business well, meeting the needs of the markets it serves.

And in time, every business goes the way of the buggy whip.

So increasing its profits is not the universal social responsiblity of business, but it is the universal need of Enterprise Finance through securities trading.

This conflation of business, as a social supplier of choices to popular choice, and the corporation as a financing agreement with Exchanges & Funds was further normalized into the prevaling social narrative in the next following year, 1972, when Lewis Powell authored a memornadum for the United States Chamber of Commerce, on The Attack on the American Free Enterprise System.

Through this Memorandum, Free Enterprise became conflated with Corporate Power, and so also, the power of the securities trading markets, to monopolize the values that get valued in business and the economy, and through the economy, in society, social policy and Politics.

See for example, the way Powell, in his Memorandum, identifies Consumer Advocate Ralph Nader as a chief enemy of “American free enterprise”, citing a profile published in Fortune Magazine, that actually described Nader as an opppenent of Cporate Power (not free enterprise).

In the year following the Powell Memordum, in 1972, the National Commission o Unifrom State Laws, a volunteer lawyer organization in the United States tasked with recommending unifrom laws to reconcile idiosyncratic differences in local laws acros the several states in the United States that hindered an increasing national and supra-national economy and social order, promulgated the Uniform Management of Institutional Funds Act, recommending, effectively, the codification into law of the conclusions eached by Cary and Bight in their 1960 Report to Ford Foundation.

This cleared the way for securities trading markets professonals to seize control of the rapidly growing sums of society’s safe money that was being aggregated into the Mid-Century Modern social innovation of the social trust for provisioning mutual aid societies for Workforce Pensions, transforming fiduciary stewards of a dignified future for so many, directly, as a private benefit, that it is also for us all, consequently, as a public good, into Asset Owners financing Corporate Power through Profit Extraction from Growth in Selling Price.

That, we now know, is not a good thing.

So, what can, should and will we do about it?