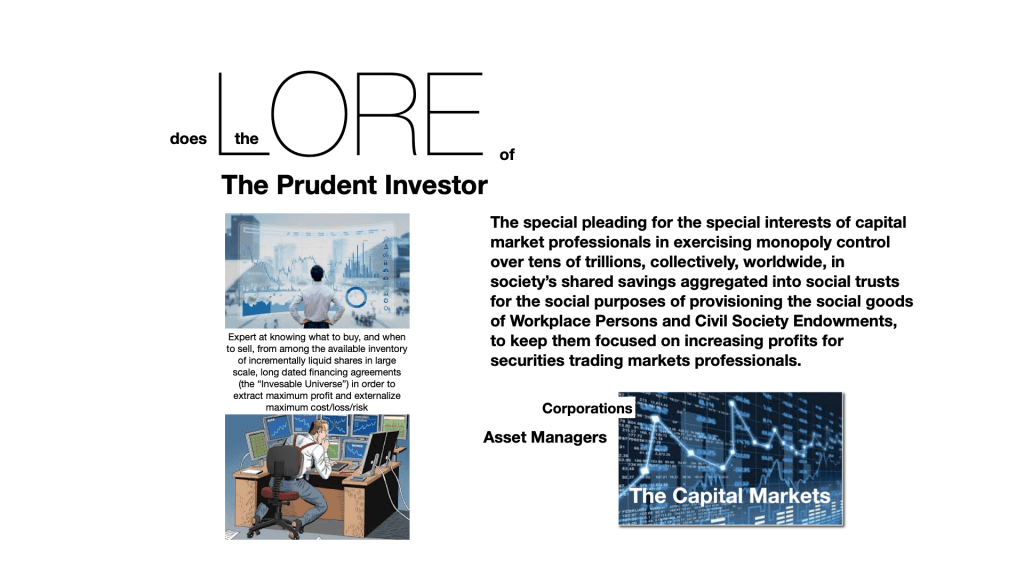

Since the 1970s, securities trading makets professionals

“

have basically pushed out the attorneys from interpreting fiduciary duty

– Keith Johnson

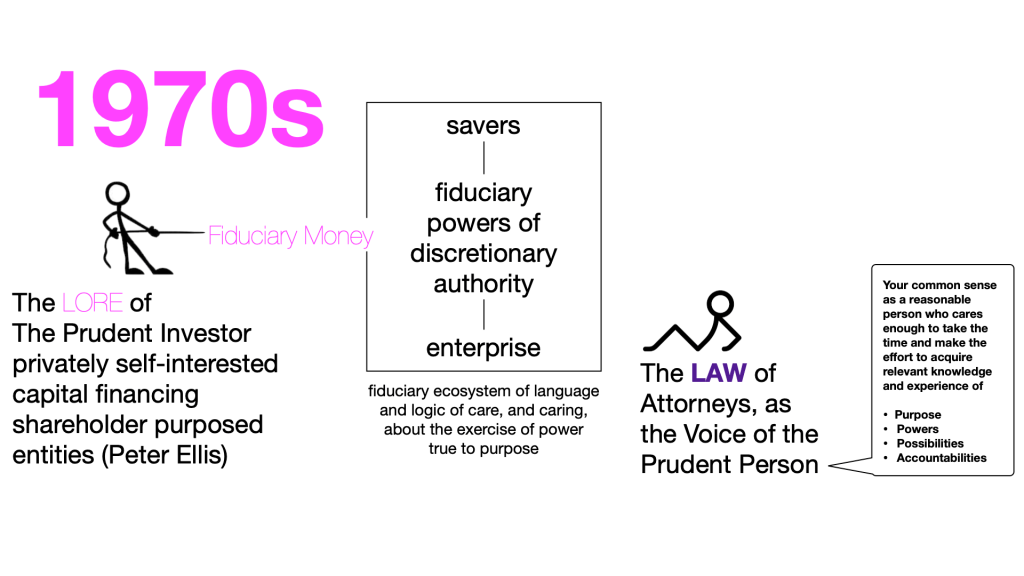

Empowered by the Uniform Managment of Institutional Funds Act, that re-asserted the law of prudence aginst the lore of the Legal List, securities trading market professsionals have succeeded in replacing the Prudent Person, familiar with such matters, with the Prudent Investor, expert at managing pricing risk in the securities trading markets.

This pushed out attorneys, as experts in the law of trusts, and avatars for common sense, and put in charge experts in securities trading.

This is a problem, for society and the economy, for Pensions & Endowments and for the Exchanges & Funds.

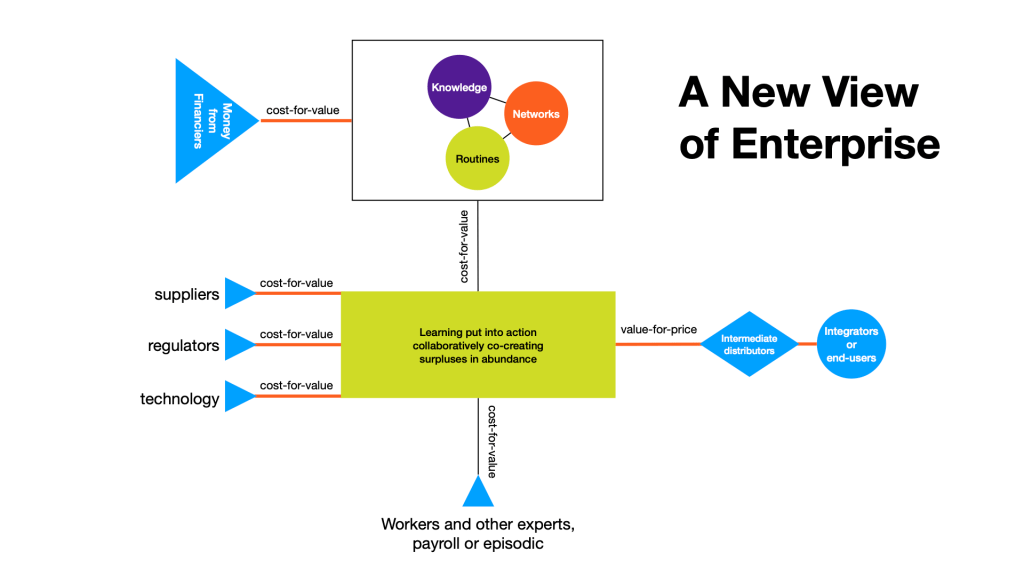

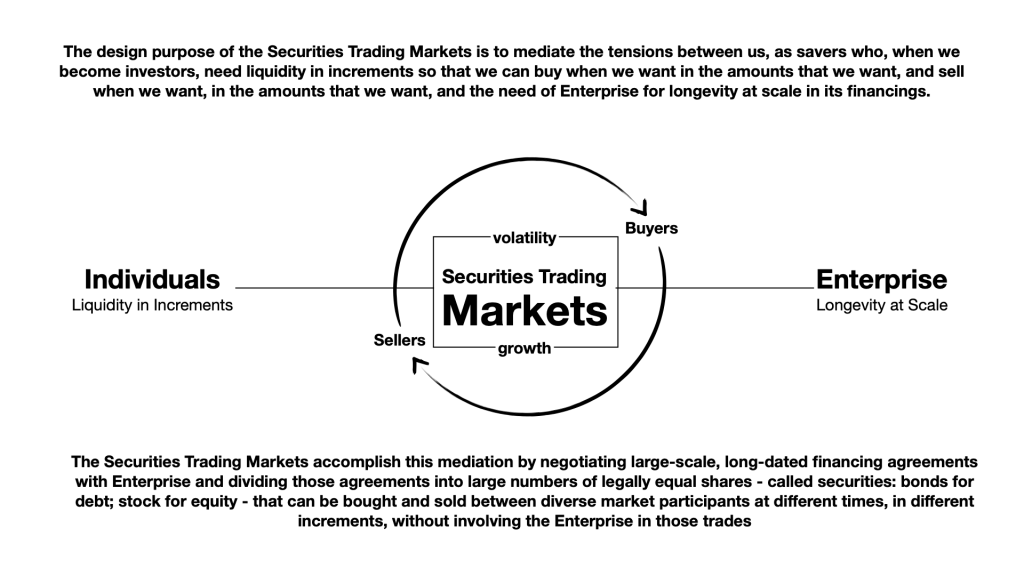

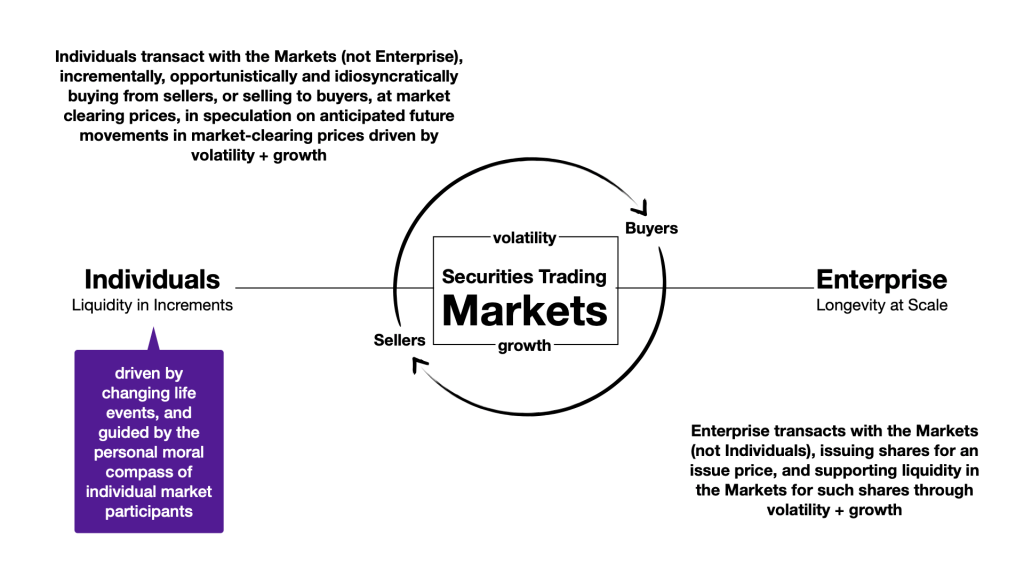

The problem is that the securities trading markets are created by design to mediate the tensions between our need as individuals, for liquidity in increments in our investments and the need of enterprise for longevity scale in their financings.

As individual savers, we need to be able to invest whatever amounts we want, for however long we want, and to get all or some of the amounts we have set aside for investment back, whenever we need or want them back, to spend on something else.

Enterprise needs to repeat on a regular and recurring basis its work of transforming cost-for-value into value-for-price, to honor its social contract with popular choice.

The securities trading markets mediate those tensions by:

- agreeing large-scale, long-dated financing agreements with Enterprises;

- securitizing those agreements by breaking them up into large numbers of small, legally equal commodity shares of ownership

- Bond, for debt

- Corporate stock, for equity

- various kinds of ownership interests in various kinds of portfolios of commercial paper (short term corproate loans), consumer debt (home mortgages, credit cards, automobile loans and leases, student loans, etc.), securities trading strategies (mutual funds), interest and exchange rate (currency) swaps and other derivatives and hedges, marketed as innovative financial products

- issuing those shares of ownership at market clearing prices to participants in the markets for maintaiing market-clearing prices on such shares

Shares listed for trading in the markets can be bought and sold by individuals as market participants, at whatever times and in whatever quantities at whatever prices, without involving the issuer in those transactions.

The markets manage this trading activity while the issuers keep their capital in their businesses, according the terns, legal and implied, of their agreement with the markets,

The markets themselves are concerned only with trading volume, which requires minimum levels of volatility and growht in market clearing prices, to ensure that every market participant that wants to sell can find a buyer willing and able to buy, at a market clearing price, and every market participant that wants to buy can find a seller wiling and able to sell, at a market clearing price.

In order for a buyer to be willing to buy, sellers have to be seen as selling at a profit.

Profits can be taken from volatlity – short term fluctuations in the market clearing price; or from growth – long term increases in the market clearing prices.

For bonds/debt and bond-equivalents, profit extraction is exclusively from volaility, because the terms of the underlying loan are fixed, and do not. Volatility in debt securities can be driven by changes in supply and demand between buyers and sellers, and by market perceptions of value associaed with changes in prevailing rates of interest, the credit rating of the issuers and other such “fundamental” considerations.

For corporate stock/equity and stock-equivalents, profit can be extracted from volatility, driven by considerations analogous to the drives of volatility in the debt markets, but more importantly, from growth in the market clearing prices for corporate shares (and equivalents) reflecting increases in the net present value (NPV) of the free cash expected to flow through the hierarchical managemnt bureacracies of the issuing corporation (or equivalnet legal entities), and speculation about how other market participants expectations for growth in market clearing prices will drive movements in th emarket clearing price.

The markets themselves do not set the prices. Prices are set by market participants through a biddding process knows as the Dutch Auction Method.

Market makers collect bids, from market participants wanting to buy, and asks from market particpiants willing to sell, and when they get a match (after adusting for a “spead”, which is their profit for making the market) they make the sale, settling the transaction (collecting payment and delivering shares) after the fact.

When individuals enter the markets, decisions about when to buy and when to sell are driven primiarly by changing life events outside of the securities trading markets: we buy when we have some moey to “take a chance” with, and sell when we need that money back, for some other purpose. Decisions on what to buy and sell are driven mostly by perceptions of possibilities for extracting a profit, constrained by our own personal moral values, and guided by our own individual moral compass.

The makets themselves have no moral compass – they are amoral; but market participants do.

And that is what give the markets their morality, as the combined moral values of so many individual market participants that it a close-enough approximation of the moral values of society, more generally, relative to which businesses should be supported in doing business through Finance, and how those busiensses should be supported through Finance in doing business.

[There is a corrollary accountability of business to popular choice and shared morality in the commercial markets for Enterprise and exchange.]

However, when instittions like Pensions & Endowments come into the securities trading markets, the dynamics of market morality change.

Pensions & Endowments are self-perpetuating “forever machines” that have no life events that determine when they buy and when they sell. They always have to be invested. That’s their job. They are financiers in their own right.

Over time, they do receive additons to their “corpus” (the legal term for the money they own, as stewards, care-takers and fiduciaries), and when they receive more money, they do have to put that additional “corpus” to work, making new investments.

They also have a legal obligation to pay out actuarial or fiduciary sums to the Pension or Endomwent they support, according to the terms of their constitutig documents. This is usually a percentage of the corpus, and typically ranges between 6-8% each year.

That’s it.

That’s their cash flow managment dynamic. Mostly, they have vast sums of money entrusted to their plenary powers of discretionary authority that they have to put to work, making through investing at least an actuarial/fiduciary cost of money, while protecting principal (another word for “corpus”, borrowed from the financial lexicon of debt finance) against loss.

Once they buy into the securities trading markets, they never really need to sell, unless something adverse has happened to the underlying issuer that alters the market value of their securities, requiring a sale to minimize or avoid a loss.

Large amounts of this “once we buy, we never have to sell” “foever” money flowing into the securities trading markets, which started in the 1970s, creates problems for those markets.

All this money buying and not selling would become a weight on the markets, reducing transaction volumes, and impairing the abiity of the markets to deliver liquidity to market participants (and the ability of securities trading market professionals to earn fees and profits on transaction volumes).

A solution was found in the work of Harry Markowitz and his theories of portfolio diversification across uncorrelated trading positions to manage the risk of pricing cyclicality, and realize across a suffient large and well-diversidied portfiolio an return that “meets or beats the market”.

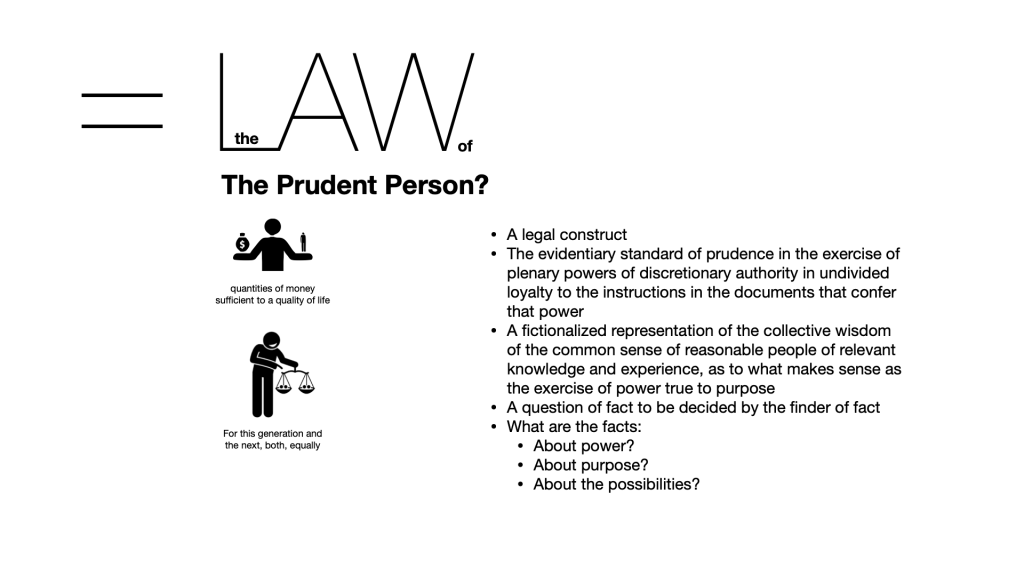

What we now know as Modern Portfolio Theory was seized upon as a prudent reason for fiduciaries to trade; to manage risk, for the safety of their portfolio.

Safety is one of the two goals of every trust. The other is income.

“

income as well as safety”

– Samual Putnam, Harvard v. Amory

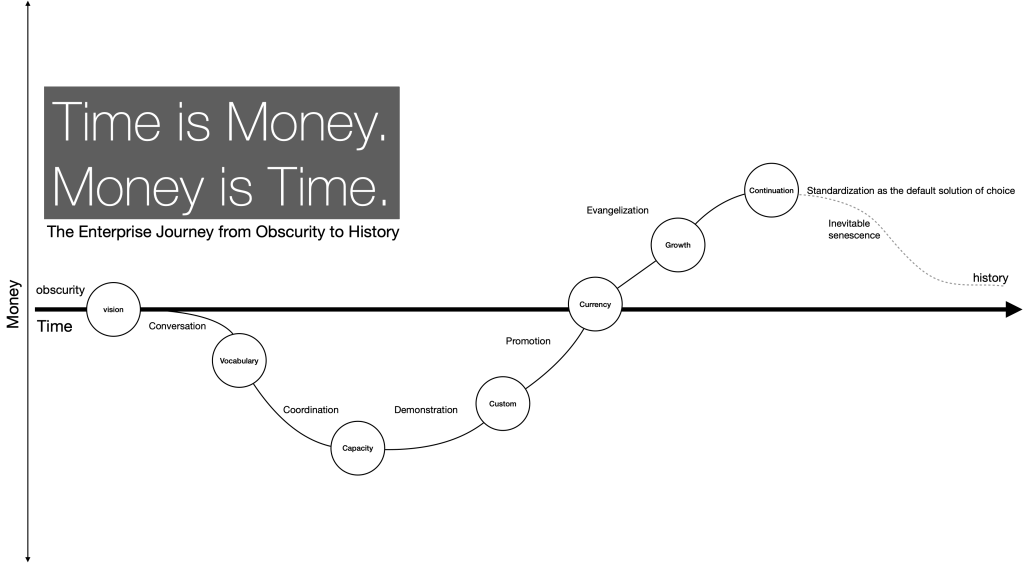

Over time, through conversation, a new vocabulary was constructed.

The Prudent Person (see Putnam, in Amory, above) became the Prudent Investor.

The Prudent Investor become the Institutional Investor.

Trading positions in the securities trading markets became Assets.

Fiduciary stewards of social trusts became Asset Owners.

Different securities traded in different securities trading markets, and different strategies for trading different securities in different securities tradign markets became Asset Classes.

Securities trading markets professionals who made themselves expert at diversifying portfolios of trading positions in the securities trading markets, by applying (or evolving, or ignoring) the principles of Modern Portfolio Theory became Portfolio Managers.

Portfolio Managers became Asset Managers.

Asset Owners and Asset Managers became Institutional Investors.

The take over was complete. All separation between securities trading through Exchanges & Funds and society’s “safe” money aggregated into self-perpetuating social trusts as “forever machines” for sustaining the new commons of Workforce Pensions and Civil Society Endowments was dissolved.

All accountability for prudence and loyalty to the purpose of these new commons was lost, replaced by loyalty to Growth in Gross Domestic Product (GDP) that powers Growth in the Net Present Value (NPV) of cash flowing through the hands of corporate bureuacrats, and the selling prices of corporate shares, that powers Growth in the Net Asset Value (NAV) of trading positions in the securtities trading markets, that powers Growth in Assets Under Management (AUM) by Asset Managers that powers Grqwth that powers Growth in fees and profits for securities trading markets professionals and participants.

Along the way, the securities trading markets became the Capital Markets, which became the Financial Markets, which became, just the Market.

The securities trading markets became both a perfect proxy for the economy, and a perfect point of intervention in the economy: if “the Markets” are up, all is well in the world; so humanity MUST do whatever is necessary to ensure that the Markets keep going up!.

This became THE measure for success at being human:

In this way, we have become shackeld, not just in the US, but across the planet, to a locked imginary that Growth as the simple quantitative increase in qualitatively undifferentiated transaction volumes measured in numbers, as prices paid in money, is both necessary and sufficient to our fulfillment as Humans as the Masters of Nature, through the on economy as the production and distribution of goods and services through makets for allocating scarcity through price, that calls on each of us, and all of us, to work hard to produce and consume more, so that the Markets can give us more, on the promise that:

- this “more” will also always be better; and

- we each, as freely self-determining market participants [participants in which market? the commercial markets; or the securites grding markets?] will always be free to determine, each for ourselves, our own fair share of this more that is always also better.

The corrollary of this, spoken, if at all, only in low voices, among “the right people”, is that success in the Markets is proxy for worth as a person: if you have money, that means you are morally upright and deserving; if you don’t have money, well that means you are is some way morally deficient and undeserving.

Here, again, quality does not matter. Quanitity does.

It does not matter HOW you got your money, it only matters THAT you have money. That always means that you are morally superior and deserving.

It does not matter WHY you don’t have money. What circumstnaces and conditions beyond your control have schackled with with obstacles and disadvantages. It only matters THAT you do not have money. That means you are in some way for which you alone are fully responsible, in some way morally inferior and undeserving.

Two problems with this.

One, it is not true.

Two, Nature does not agree.

Lived experience teaches that it is as much about “the luck of the draw” and “the cards we were dealt” as it is about hard work and moral discipline, how much many any one of us comes to exercise control over in our own personal journy through life. It is true that hard work and more discipline can make more of less. It is not ture that just becuse you have more, that you are deserving of what you have, or in some way better than others for having it.

Also, Growth comes with consequences, and if we recklessly choose not to reckon with those consequences, life will get worse, and not better.

And so, the morality of the Markets, which leaves it to others to deal with the consequences of endlsess profit extraction from endless growth in selling prices, is a morality that always leads to episodic catastrophe.

What Corporate Capture of Fiduciary Money promises is endless riches for the morally deserving.

What it actually delivers is:

- short-termism

- market elitism